Business Day

Your Mutual Fund

Has Your Proxy, Like It or Not

Fair Game

By

GRETCHEN

MORGENSON

SEPT.

23, 2016

Do you

think executive compensation is out of control or that a company

should have to disclose its political contributions?

If so,

you may also think that your mutual fund should vote on these and

other issues in accordance with your beliefs. Good luck with that.

As investors, we

are supposed to be able to sound off on corporate governance matters at the

companies whose shares we own. We do so by voting on the issues when they arise

at a company’s annual shareholders’ meeting.

But if you invest,

as most people do, with a large fund manager, like BlackRock or the Vanguard

Group, the chances are very good that your objections to common corporate

practices are not getting through. That is because fund overseers vote your

shares and often do so without regard to your views.

The result is a

breakdown in one of the few accountability mechanisms available to individual

investors in our so-called ownership society. This failure has everything to do

with the fact that executive pay rises higher each year.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

The voting of fund managers is infected by conflicts of interest, said

Erik Gordon, a professor at the

Ross School of Business at the University of Michigan. That is because

these giant mutual fund operators don’t just own shares in many big

American companies; they also do business with them.

“Funds

often avoid challenging management on executive pay and corporate

governance because they want to be included in corporate

defined-contribution benefit plans,” he said in an email. “If a fund

irritates a C.E.O. and the C.E.O.’s pals on the board, the fund risks

losing business at several companies.”

BlackRock and

Vanguard dispute this notion, saying they put their customers’ interests first

in their voting. “We weigh all factors that could affect the long-term value of

our clients’ assets,” Ed Sweeney, a spokesman for BlackRock, said in a

statement, “including the hundreds of public pension plans, nonprofits,

foundations, endowments, educational institutions and individual investors we

serve.”

Every August, fund

companies must disclose how they voted in the most recent proxy season. I asked

Proxy Insight, a data analytics firm that

tracks such votes, to tally those of

BlackRock, with almost $5 trillion in

assets, and

Vanguard with over $3 trillion.

Here is what I

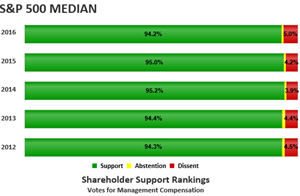

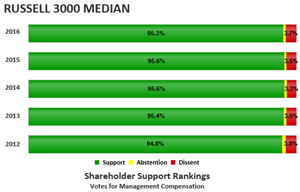

learned. On matters involving executive pay, in the most recent 12 months, both

fund managers overwhelmingly supported compensation practices at the companies

in the Standard & Poor’s 500-stock index. BlackRock supported executive pay at

98.3 percent of those companies in the most recent year, and Vanguard voted in

favor of pay practices in 98.1 percent of its votes. (Vanguard disputed this,

saying it voted yes a mere 96 percent of the time.)

By the way, both

companies supported the pay practices at Wells Fargo, whose executives

are under fire for overseeing

a pervasive program that prompted many

employees to set up sham accounts to generate fees and make quotas.

As head of

BlackRock’s investment stewardship unit, Michelle Edkins oversees its voting. On

executive compensation, she stressed that the firm voted against pay practices

or compensation committee members at 10 of the 50 companies with the

highest-paid chief executives this year. She also said that BlackRock discussed

compensation matters with half of those companies.

Beyond pay,

BlackRock and Vanguard both supported management by voting against most

proposals requiring that a company’s board be led by an independent chairman.

Shareholders in favor of this idea contend that such a move would reduce

management’s grip on the board and bring more accountability to corporations.

BlackRock voted

nay on 95 percent of such proposals, Proxy Insight found, while Vanguard

rejected 100 percent of them.

That is not

particularly surprising, given that neither BlackRock nor Vanguard has an

independent chairman overseeing their boards. Laurence Fink is both chairman and

chief executive at BlackRock; F. William McNabb III holds both titles at

Vanguard.

Officials at both

companies said they voted against independent chairman proposals at companies

whose boards had lead independent directors and whose roles brought necessary

balance to the boardroom. BlackRock and Vanguard themselves have lead

independent directors on their boards.

Nevertheless, a

lead director will rarely be as powerful as an independent chairman.

The actions of

BlackRock and Vanguard stand in contrast to some other big fund managers.

AXA Investment Management, with $760 billion

in assets, voted in favor of all independent chairman proposals in the most

recent year, Proxy Insight said. And

RBC Global Asset Management, with $300

billion, supported 97.5 percent of them.

Another type of

proposal nixed by both BlackRock and Vanguard would require companies to

disclose their political contributions and lobbying expenditures. Ms. Edkins at

BlackRock characterized such proposals as micromanaging but said, “We believe it

is the responsibility of the board to ensure there is a robust process around

any type of spending that has a reputational impact on the firm.”

By contrast,

Deutsche Bank Asset Management, with about

$800 billion in assets, and

Pax World Management, with $4 billion in

assets, voted in favor on 95 percent of those proposals.

Neither BlackRock

nor Vanguard is a stranger to lobbying. During 2015 and so far this year, the

Center for Responsive Politics found,

BlackRock spent $3.73 million lobbying Capitol Hill on financial regulations and

Vanguard spent $3.38 million.

Deutsche Bank

spent considerably less — $900,000 — and the database showed no expenditures for

Pax World.

Asked about these

and all their votes, both BlackRock and Vanguard cautioned that they were just

one way of communicating their views to companies. Company officials said they

also regularly discussed issues of concern with boards and if they got nowhere

would vote nay. BlackRock voted against 5 percent of directors up for election

this year at the approximately 4,000 companies whose shares it owns, Ms. Edkins

said.

Vanguard abstained

on almost 20 percent of shareholder proposals this year. One required companies

to report on the gender pay gap among employees. Vanguard abstained on this at

Alphabet, Citigroup, Danaher and eBay, among others.

In a statement,

John Woerth of Vanguard said the company generally abstained from voting on

social or environmental proposals that it did not believe “have a clear link to

increasing shareholder value.” Vanguard will engage on topics that could affect

long-term value, like climate change, he added, “to understand their processes

for overseeing and managing those risks.”

One of Vanguard’s

abstentions involved pay. A shareholder proposal at the Ameren Corporation, a

big utility in the Midwest, would have required its top executives to hold on to

a significant number of shares for two years after leaving the company. Such

programs align pay with shareholders’ interests by encouraging executives to

manage for the long-term.

About 50.6 percent

of shares were voted against the proposal versus 35 percent in support. Had

Vanguard voted its 22 million shares in favor, the proposal still would have

failed. But the vote would have been close enough that Ameren’s management might

have been forced to take the proposal more seriously.

Vanguard declined

to comment on this abstention.

Mutual fund voting

practices that perpetuate the status quo are on the agenda at a daylong

symposium on Sept. 27 in Washington. The

event, called “Breaking Through Power,” was convened by the Center for the Study

of Responsive Law, a nonprofit founded by Ralph Nader, who has strong views on

fund managers’ voting.

“Mutual funds are

a top-down autocracy. How can they be expected to go after the corporations

they’ve invested in when there is such conformity of abuse?” Mr. Nader asked.

“If they criticize executive compensation, they have to look at their own

executive compensation. If they deal with corporate disclosures they’re going to

have at look at their own disclosures.”

Unfortunately,

there is little that investors can do to change this dynamic.

But here is an

idea. If your fund company votes the wrong way on issues you care about,

register your displeasure by voting against the fund’s directors in its annual

election. Maybe that will get someone’s attention.

A version of this article appears in print on September 25, 2016, on

page BU1 of the New York edition with the headline: Your Fund Has Your

Say, Like It or Not.

© 2016 The

New York Times Company