Business Day

EpiPen Price

Increases Could Mean More Riches for Executives

Fair Game

By

GRETCHEN

MORGENSON

SEPT.

1, 2016

|

Heather Bresch, chief executive at Mylan,

which has found itself at the center of the latest public

outrage over high drug prices.

Credit Victor J. Blue/Bloomberg |

Heather

Bresch, chief executive at

Mylan, the pharmaceutical giant

that has been vilified for price increases on its EpiPen allergy

treatment, maintains that her company has attained a sort of

capitalist nirvana — it does

good for others while doing well for itself.

But the

argument that

Mylan has achieved a balance

benefiting all of its stakeholders simply doesn’t hold up when viewed

through the prism of the company’s recent proxy filings. Those

materials detail the company’s

executive pay and show, for

example, that Mylan’s top brass received a windfall when it

incorporated overseas in 2014 to cut its tax bill sharply.

The filings also

show that under a special, one-time stock grant created in 2014, top executives

— including Ms. Bresch — stand to reap further riches at least partly on the

back of price increases on the EpiPen. Under the grant, Mylan executives will be

rewarded if the company’s earnings and stock price meet certain goals by the end

of 2018.

Given that EpiPen

accounted for $1 billion of Mylan’s $9.4 billion in revenue in its most recent

year, the allergy treatment’s price increases seem integral to meeting those

targets and generating a big payday.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

Mylan says the one-time grant aligns management’s interests with those

of the shareholders. But relentlessly managing a company with an eye

toward its stock price can lead to trouble.

In any

case, the timing of the one-time stock grant to executives is striking

— especially when set against the history of EpiPen price hikes.

According to

Truven Health Analytics, Mylan began

significantly stepping up the pace of its EpiPen price increases just a few

months after the company announced the special grant in February 2014. While

price increases in the previous four years averaged 22 percent annually, in 2014

and 2015 Mylan increased EpiPen prices 32 percent each year.

I asked Mylan if

the bigger price increases after the 2014 stock award were intended to help

propel its performance toward the earnings and stock price targets.

No, replied Nina

Devlin, a spokeswoman.

In a statement,

she elaborated further: “Mylan has a large and diverse business, with more than

2,700 products sold in 165 countries and 600 products sold in the U.S. alone.

The targets set forth in the one-time special program were not and are not

practically achievable based on pricing of any single product.”

Ms. Devlin added

that after Mylan’s recent acquisition of Meda, a company specializing in women’s

health, respiratory, allergy, dermatology and pain management, the EpiPen

business will represent under 10 percent of the company’s revenue, compared with

11 percent last year.

But Brian Foley,

an independent compensation consultant in White Plains, said it was impossible

to separate the company’s business decisions from its pay practices. “The

pattern of conduct with the EpiPen business seems egregious,” Mr. Foley said in

an interview. “It looks like price gouging, and why would you do that? The

answer has got to be because it’s in management’s financial interest to do it.”

Consider the

special stock award. In 2014, Mylan’s proxy filings valued Ms. Bresch’s grant at

$13.2 million. If Mylan clears the price and adjusted earnings hurdle, her

payout will be far larger.

Now, though, with

Mylan’s pricing practices under scrutiny, it may be more difficult for the

company’s executives to clear the hurdles necessary to cash in. Its stock is

well below the $53.33 price that will be needed to generate a payout. And the

company’s decision last week to start selling a generic EpiPen at half the $600

branded price means the adjusted earnings per share target of $5.40 on Dec. 31,

2018, may be more difficult to achieve.

But don’t cry for

Ms. Bresch. It turns out the earnings hurdle put in place by the board has some

wiggle room. That’s because it is based not on generally accepted accounting

principles but on a so-called adjusted earnings figure that excludes certain

corporate costs chosen by Mylan. The company also uses fantasy figures when

calculating its top executives’ incentive pay packages.

Among the costs

Mylan excludes from its adjusted earnings are those related to acquisitions,

financing and investment losses. Last year, these and other exclusions gave a

big boost to Mylan’s pretend per-share earnings. Under generally accepted

accounting principles, each Mylan share earned $1.70 in 2015. Under its own

rules, each share earned $4.30.

That spread

between Mylan’s actual earnings and its pretend number — $2.60 a share — has

widened significantly. In 2014, it was $1.22 a share.

Note, too, that

Mylan’s true earnings in 2015 were 27 percent below what it actually earned in

2014. Luckily for Mylan’s top executives, earnings as computed under accounting

rules are not one of the company’s metrics for calculating executive pay.

Ms. Devlin, the

Mylan spokeswoman, contends that its preferred financial measures are “useful

supplemental information for our investors” in addition to those presented under

accounting rules. She added: “All public companies in our peer group use non-GAAP

measures, as do a large number of public companies outside of our peer group.

Furthermore, the board and/or compensation committee has discussed these metrics

with shareholders and has taken that feedback into consideration.”

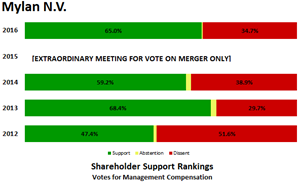

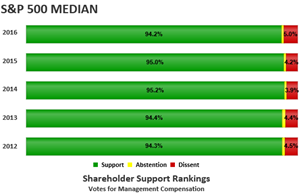

At Mylan’s most

recent annual shareholder meeting, 35 percent of the votes were cast against the

company’s pay practices. By contrast, the median company in the Standard &

Poor’s 500-stock index received support from 95 percent of votes cast.

On Thursday, Scott

M. Stringer, the New York City comptroller and overseer of city pension funds

that hold Mylan shares, criticized Mylan’s governance practices in a letter to

Douglas J. Leech, chairman of the nominating and governance committee of the

company’s board. Mr. Stringer, who has voted the city funds’ shares against

Mylan directors in the past, asked that the company install an independent board

chairman to provide oversight.

We’ll have to wait

until December 2018 to see whether Mylan’s executives can cash in their special

one-time awards. In the meantime, Ms. Bresch and her colleagues received a

windfall after the company acquired certain businesses of

Abbott Laboratories in 2014 and

incorporated overseas. As part of the deal, executives were allowed to exercise

all their unvested stock awards. Ms. Bresch realized $32 million in 2015 as a

result, proxy filings show.

That’s not all.

The company also paid its executives’ income taxes associated with the

acceleration of the stock awards. Under that deal, Mylan shareholders paid the

extra $5.8 million Ms. Bresch owed in taxes.

The outcry over

the EpiPen pricing shows Mylan to be the latest example of a company whose board

allowed executives to reap bounties from activities that wound up harming other

stakeholders. When they do so in the name of the company’s shareholders, it is

especially offensive. And now that Mylan has reminded everyone just how common

price gouging is in the pharmaceutical industry, even its shareholders are

paying a price.

“You would think

at least somebody on the board would have the brass and the class to say enough

is enough,” Mr. Foley said. “We were making money at $400; why do we need to

charge $600? This reminds me of my 16-month-old grandson who after he’s had a

good meal looks at me and says: ‘More?’”

A version of this article appears in print on September 4, 2016, on page

BU1 of the New York edition with the headline: EpiPen Soars and So

Does Bosses' Pay.

© 2016 The

New York Times Company