|

Editor’s Note:

Allen He is

a Director, and Jessica

Pollock is

a Research Associate at FCLTGlobal. This post is based on their

FCLTGlobal memorandum. |

Data from year-end

2022 shows

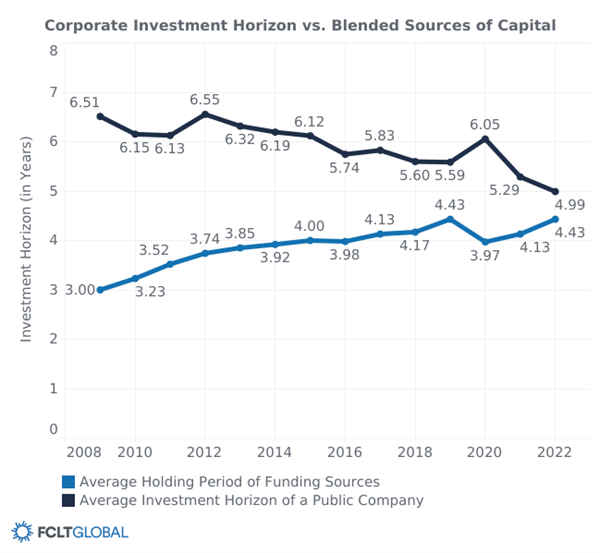

the investment horizon gap between companies and investors [1] remains

slim, though for the first time since our tracking began, investors

are leading with longer investment horizons than companies. On paper,

closer alignment of investment horizons between providers and users of

capital may appear to be a positive development for value creation in

capital markets. However, ‘closer’ doesn’t necessarily equal ‘better’.

While the past year reflects a continued long-term upward trend in

investor horizons, it also revealed a material decline in investment

horizons for corporates. This raises questions about the potential for

corporates’ long-term value creation. Specifically, the material

reduction in corporate investment horizons over the last two years

brings them to their lowest value since FCLTGlobal’s tracking began.

Furthermore, the increasing horizons can be attributed more to changes

in portfolio composition than to a fundamental shift in investment

behavior. It is important to note that the effects of these trends

vary significantly across geographies, sectors, and even within asset

classes. We highlight a few of the key drivers in corporate and

investor investment horizon changes below.

Companies’ investment horizons shortened in 2022

Companies in 2022 underwent a notable shift in investment strategies,

resulting in companies shrinking their investment horizon. This

reduction, from 5 years 4 months in 2021 to 5 years in 2022, was

primarily driven by two key factors: an upsurge in buybacks and a

decrease in retained earnings. As businesses increasingly opted to

repurchase their own shares and allocate fewer funds to retained

earnings, they experienced a shorter-term orientation to capital

deployment. This shift reflects a changing landscape, indicating a

stronger emphasis on immediate return of capital to investors in the

corporate world.

Spotlight on buybacks and

retained earnings

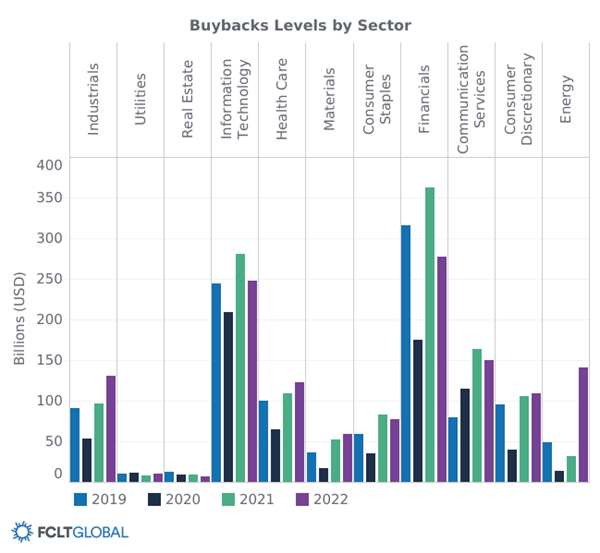

Globally in 2022, despite an overall 17% decrease in total uses of

capital, buybacks emerged as an outlier, showing both an absolute and

percentage point increase compared with previous years. Companies

reached an unprecedented high of $1.29 trillion in buybacks,

indicating a substantial upward trend compared to the curbing that

took place during the start of the pandemic in 2020. The surge in

buybacks can be attributed to favorable monetary policies and

companies’ accumulation of excess earnings and cash on their balance

sheets since 2021.

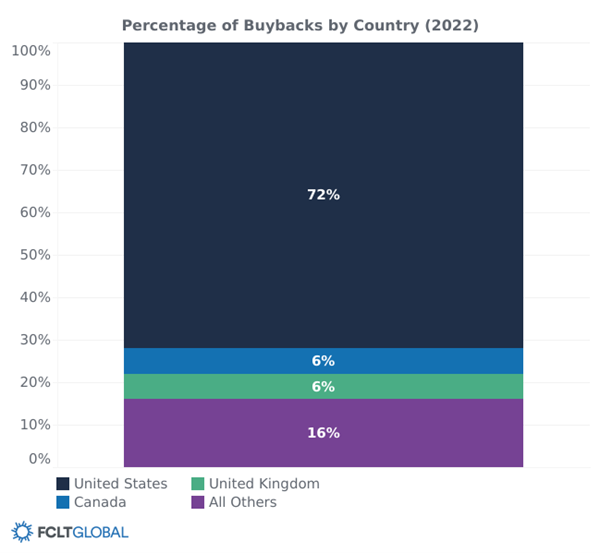

US companies have underpinned this buyback spree in recent years, as

have the Finance and Information Technology sectors globally. In 2022,

the Energy sector played an outsized role in buybacks as rising prices

generated higher earnings while fossil fuel companies continue to

implement their climate transition strategies. More broadly, this data

highlights a trend among corporates, particularly in the US, to

strategically invest in their own stocks by allocating excess capital

towards buybacks while enjoying substantial financial strength.

R&D expense, a continued bright light (but for how much longer)?

Yet recent assessments indicate that buybacks may not have been the

most prudent use of capital. According to Fortuna advisors, a

financial consultancy, the

return on investment (ROI) for buyback programs hit the lowest on

record for any five-year period since they began tracking

the metric in 2017. Additionally, buyback programs are inherently

reliant on a bullish market to produce significant value. However,

with increasing market volatility, companies need to determine whether

continued significant spending on buyback programs is the right move,

or risk over-catering towards the immediate short-term return of value

to their shareholders.

A Look-ahead to 2023

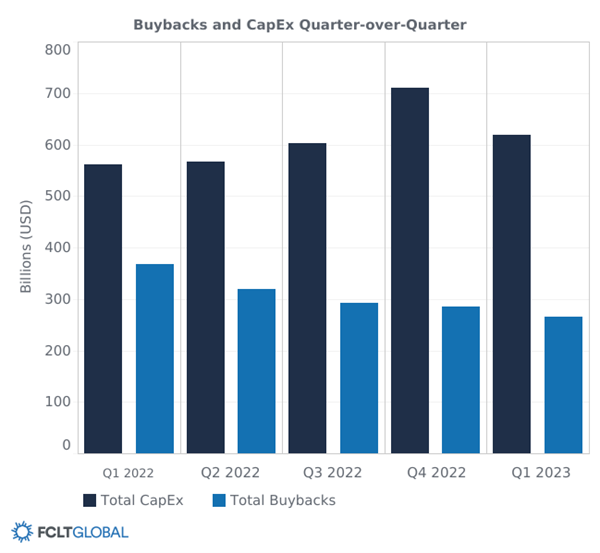

As fiscal and monetary policies tightened in the second half of 2022,

there has indeed been a slowdown in buyback activity, with the amount

spent on buybacks peaking during Q1 2022. Companies’ inclination to

“buy high” during periods of peak stock prices has also contributed to

this tapering off, and it is especially interesting that at this same

time, companies have begun spending more on capital expenditures.

Heading into H2 2023, it will be important to monitor how companies

choose to spend their capital, and its subsequent effect on corporate

investment horizons.

How the changing

environment (rising interest rates) affects retained earnings

Retained earnings and cash both decreased as earnings were deployed

elsewhere

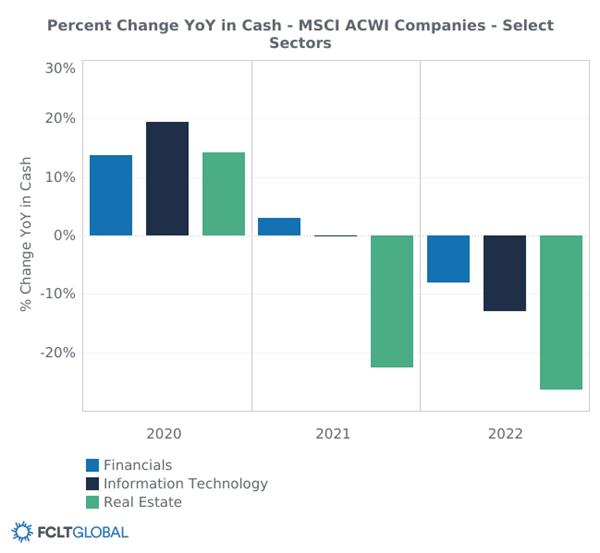

The changing economic environment has also prompted corporates to

materially reduce retained earnings in favor of other uses such as

interest expense due to rising rates. It has led corporates,

especially in sectors like financials, real estate, and information

technology, to start spending the precautionary cash reserves held on

their balance sheets for pandemic and resilience efforts over the last

two years.

This shift in uses of capital does carry risk. Less cash on hand can

mean less resilience in the event of negative shocks – as seen in the

recent collapse of Silicon Valley Bank, the Russian invasion of

Ukraine, and the pandemic. In particular, the financial sector has

seen a substantial decline in retained earnings. This might foreshadow

reduced resilience and future sector challenges, consistent with the

rise in bank downgrades and negative outlooks.

R&D expense, a continued bright light (but for how much longer)?

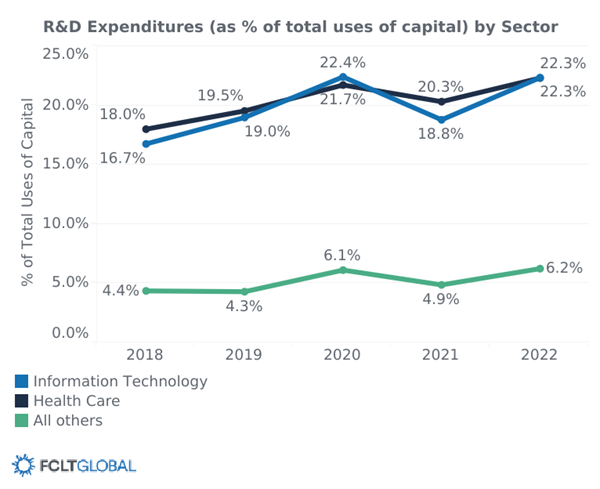

One solace for capital deployment is the continued increase in

research & development (R&D) spending, as innovation funded by R&D is

a critical driver of long-term value creation. Throughout the

pandemic, R&D spend has been the only use of capital to have increased

both in percentage and absolute value year-over-year. We see in Figure

X (chart above) that the information technology and health care

sectors have led the way, especially during the early pandemic. The

generalized boom over the past decade in R&D spending includes

spending for advancements like the human genome project, CRISPR, and

advances in AI and climate tech.

Investors’ seemed to become longer-term in 2022

Unlike their corporate counterparts, overall investor horizons

increased from 5 years 3 months in 2021 to 5 years 5 months in 2022.

However, this improvement resulted not from lower turnover and

improved long-term management practices, but from a rise in the

underlying share of indexed equities and longer duration in fixed

income instruments.

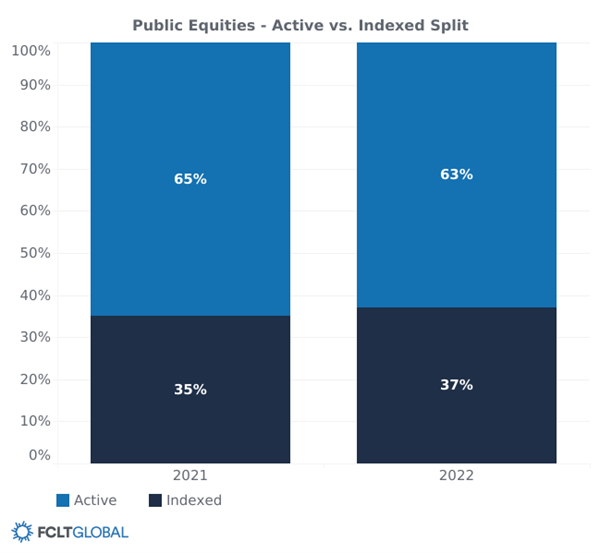

Public equity investment horizons have gotten longer-term

overall – but not due to lower portfolio turnover

Public equity investment horizons lengthened by 6 months

year-over-year between 2021 and 2022. The primary driver was a shift

in equity composition from active to indexed strategies, as the latter

have much longer investment horizons.

Here it is worth noting that turnover increased in

actively-managed portfolios as well as some indexed portfolios, which

would normally lead to shorter investment horizons.

Indeed, the downturn and turbulence in stock markets in 2022, combined

with the strategic repositioning of portfolios, led to higher turnover

in active equity portfolios investment and caused investment horizons

for these assets to decrease from 2 years 10 months in 2021 to 2 years

7 months in 2022.

In contrast to active equity, overall turnover for indexed equities is

marginally lower in 2022, implying investment horizons are slightly

higher. Underneath this aggregate number, however, the uptick in

volatility led to more major index rebalancing, with more companies

added to and removed from indexes, increasing turnover.

As such, while overall investment horizons for public equities

increased, the changes are more due to indexed

equities making up a larger portion of total assets under management rather

than any specific improvements in turnover industry practices. Fixed

income investment horizons have also increased overall – but effects

vary by subclass.

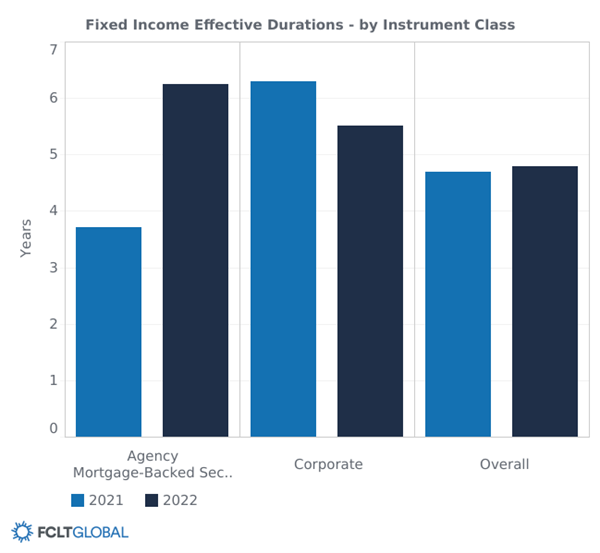

There is a similar nuance to

the fixed income investment horizons, which increased from 4 years 8

months in 2021 to 4 years 10 months in 2022. However, it is worth

noting that not all subclasses experienced a lengthening of investment

horizons and durations.

Interest rates have increased significantly across many jurisdictions

in 2022, leading to higher volatility to the asset class overall.

However, higher interest rates have notably different effects on

different subclasses of fixed income instruments.

Specifically, the durations of instruments like mortgage-backed

securities and asset-backed securities tend to increase as rates rise

due to lower expected prepayments. We see that MBS durations have

indeed increased from 3 years 9 months in 2021 to 6 years 3 months in

2022. By contrast, higher interest rates for corporates tend to have

the opposite effect, as it becomes more costly to roll over debt and

companies look to alternative sources of capital. We do see that

corporate durations have decreased from 6 years 3 months in 2021 to 5

years 6 months in 2022.

What to make of the horizon

gaps?

Narrow gaps and longer horizons aren’t necessarily indicators of

strategic long-term behavior

The data indicates that corporates are adopting shorter-term

investment strategies and alarm bells should be ringing. Though the

gap between the investment horizons of corporates and investors

remains small, and investors appear to have gotten longer-term in

2022, this doesn’t necessarily imply a positive change, as it may not

reflect longer-term behaviors on the part of investors. Overall, it is

essential for both corporates and investors to carefully evaluate

their strategies to ensure they align with long-term value-creation

and financial resilience.

Endnotes

1This

data only includes asset managers as this data is currently available.

The savers data (i.e. pensions, insurance companies, households, SWFs

etc.) typically come out later in the calendar year. Check back here

in December for fully updated information.(go

back)

|

Harvard Law School Forum

on Corporate Governance

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2023 The President and

Fellows of Harvard College. |