Driving the Conversation: Long-Term

Roadmaps for Long-Term Success

Posted by Ariel Fromer Babcock, Allen He,

and Victoria Tellez, FCLTGlobal, on Wednesday, March 6, 2019

Despite clear evidence that investors

prefer long-term communications focused on a few key drivers of

performance, companies remain mired in information demands from all

sides. Long-term roadmaps are a form of investor communication that

brings together a unified articulation of how a company will create

long-term value with the most relevant metrics to track long-term

performance. They have a proven record at leading companies, and

evidence suggests that the majority of investors (especially long-term

investors) prefer this approach. By focusing on key elements of

performance such as competitive advantages, long-term objectives, and

a strategic plan matched with clear capital allocation priorities,

companies can build buy-in among long-term investors who support a

focus on long-term value creation.

Why Long-term Roadmaps?

Survey after survey indicates that investors prefer forward-looking, long-term

guidance around a company’s strategy and expected performance.

This

post, which represents the collective effort and experience of FCLTGlobal’s

Members, academic experts, and other investment leaders, suggests a way to shift

the investor relations conversation from quarterly “hits” and “misses” toward

how companies create long-term value.

Today’s companies face increasing pressure to respond to information requests

from all sides. It is no surprise that managers and investors are frustrated.

Transitioning away from the quarterly treadmill toward conversations centered on

the long term can simplify investor communications, while simultaneously

strengthening companies’ longer-term shareholder bases, alleviating short-term

pressure and improving the accuracy of valuations. Long-term roadmaps are the

key to this transition.

Long-term roadmaps present a unified view of how a company will create long-term

value with the most relevant metrics to track long-term performance. This format

provides investors with a distillation of a company’s core drivers of growth and

competitive advantages, a company’s long-term objectives and the strategic plan

for achieving them over three to five years, and a company’s priorities for

capital allocation and investment. A long-term roadmap also off investors a

current snapshot and forward-looking trajectory of the company’s performance on

the operational and financial metrics most closely tied to growth. It focuses on

the information that investment decision makers actually need.

Two

additional factors distinguish long-term roadmaps from traditional investor

communications. First, a roadmap’s forward-looking estimates all focus on

objectives one year out, at a minimum. The point is to help investors keep the

company accountable to its plan for long-term value creation, not to provide

fodder for short-term traders and the media. Second, these roadmaps are intended

to foster dialogue between companies and long-term shareholders, rather than

serving as press releases for transient traders. Long-term roadmaps provide the

right kind of shareholders the information they need to engage with and support

corporate managers, thus facilitating the types of long-term investments that

enable ongoing growth.

The

voices of leading investors and business leaders are clear and underscore the

strong demand for a reorientation toward the long term. For example, 93 percent

of global buy-side investors want guidance from companies on metrics longer than

one year.

Our

research shows that public companies can take simple, initial steps to begin the

transition to investor communications oriented toward the long term. As

companies gain experience and comfort with this approach, these early steps can

be easily expanded into a full long-term plan. Many of the world’s leading

companies already employ these approaches today, and their experience off an

example and path for others to follow.

The

transition to long-term roadmaps has already begun. Long-term investors can

hasten it by calling on companies in which they invest to provide long-term

roadmaps and by setting an example for how shareholders engage. With the backing

of major institutional investors, companies will be able to move forward and

pursue long-term roadmaps today.

|

Short-term guidance is not important for our evaluation for new or existing

investments because it does not relate to our long-term investment horizon.

Rather, we evaluate companies positively when they refrain from this short-term

practice, particularly when they share a long-term roadmap instead.

– Chuon-Yi Ong, Senior Vice President, Public Equities, GIC Private Limited |

What Do Investors Want?

Corporate managers have good reason to feel frustrated by ever-increasing

demands for additional information. As Mozaff Khan, George Serafeim, and Aaron

Yoon have shown, firms that perform well on immaterial metrics do not

significantly outperform firms with poor ratings on the same issues. Disclosure

of these immaterial metrics adds little to no value for investment decision

makers.

According to a study from McKinsey & Company, long-term investors own more than

70 percent of the shares of US companies. For these investors, short-term

guidance does little to inform their investment choices; they simply distract

companies and their investors from the metrics that truly matter.

The

UN-supported Principles for Responsible Investment, whose signatories represent

more than $80 trillion in investable assets, urge companies to “focus on

communicating issues and metrics that are relevant to the long-term success of

the business.” In addition, a survey of investment decision makers conducted by

FCLTGlobal indicated that 86 percent of respondents would like companies to use

a minimum three-year time horizon for forward-looking targets.

Notable business leaders voice the same sentiment. “Clear communication of a

company’s strategic goals—along with metrics that can be evaluated over

time—will always be critical to shareholders,” wrote Warren Buffett, chair and

CEO of Berkshire Hathaway, and Jamie Dimon, chair and CEO of JPMorgan Chase, in

an editorial for the Wall Street Journal. BlackRock chair and CEO Larry

Fink echoes this point. In his 2018 annual letter, he wrote, “I want to

reiterate our request, outlined in past letters, that you publicly articulate

your company’s strategic framework for long-term value creation.” Harvard

professor and former US Treasury Secretary Larry Summers agrees, “Wise corporate

leaders should give a sense of their long-term vision on at least an annual

basis. Investors who insist on such information are only being reasonable.”

Investor relations organizations also acknowledge that long-term plans with

long-term metrics are an essential investor relations tool. In fact, the US

National Investor Relations Institute (NIRI) recently amended its policies to

respond to this investor preference. As its policies now state, “NIRI believes

that an undue focus on short-term, single-point guidance is undesirable and that

all relevant audiences—primarily investors, financial analysts, and the news

media—are better served when public companies focus their guidance on their

long-term strategy and business value drivers.”

Roadside Attractions: The Benefits of a Long-term Plan

Implementing a long-term approach to investor communications offers tangible

benefits, both financial and otherwise, for participants on both sides of the

investor-corporate dialogue.

Chiefly, a long-term approach attracts long-term investors. As professors

François Brochet, Maria Loumioti, and George Serafeim demonstrate, focusing on

short-term metrics attracts transient shareholders. By contrast, companies that

focus on long-term topics in their investor communications attract and build a

long-term investor base. Building that long-term investor base is important, as

it reduces a company’s cost of equity, encourages greater fixed investment, and

is ultimately associated with higher returns.

These

plans can also help management respond in the face of short-term pressure (e.g.,

from activists). Investors that understand and believe in management’s strategy

and plan for execution are more likely to support the company through ups and

downs, serving as a buff or even potential deterrent to activist attack. As

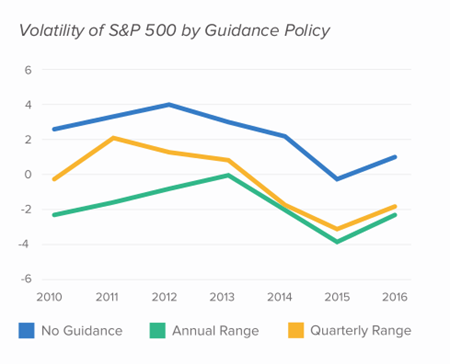

FCLTGlobal’s research on quarterly guidance demonstrates, longer-term guidance

(in this case, annual) does a better job muting share price volatility than

short-term guidance, alleviating one source of potential short-term pressure.

At

the analyst level, a long-term roadmap can ensure a more accurate valuation.

According to McKinsey & Company, 70 to 90 percent of company value is related to

cash flows three or more years out. Investor communications that don’t speak to

that horizon leave markets to fill in the blanks, often incorrectly. For

example, the 2° Investing Initiative (2°ii) found that even though financial

analysts and data providers produce forecasts for five to 10 years, companies

typically only provide forecasts for the next quarter to one year. This

disclosure gap increases the uncertainty of stock valuations by analysts, making

it more likely that the market could get a company’s future earnings

potential—and stock market valuation—very wrong.

The

benefits aren’t all financial. In addition to freeing investor relations

departments from addressing the short-term “noise” that doesn’t help their

investors, research published by Timothy Youmans and Brian Tomlinson in MIT

Sloan Management Review suggests companies that use long-term plans have

also reported better success at attracting and retaining personnel.

Similarly, managers from 66 organizations in the International Integrated

Reporting Council reported that developing and communicating a long-term

strategy delivered meaningful benefits internally: 79 percent of managers

reported that business decision making had improved, and 78 percent experienced

better collaboration between the board and management.

Speed Bumps: Overcoming the Points of Resistance

Although seemingly a simple and powerful tool, long-term roadmaps can face

resistance for both internal and external reasons. Fortunately, some of the

world’s leading companies have proven that such resistance can be overcome. When

it is, change can happen quickly, especially when investors themselves join the

effort to promote long-term planning and communications.

Interviews with FCLTGlobal’s Members and others offer a perspective on how to

address common sources of resistance. For example, many management teams are

concerned about revealing their “secret sauce” by sharing too much information

on their future plans. British pharmaceutical company GlaxoSmithKline’s (GSK’s)

vice president of investor relations, Mel Foster-Hawes, acknowledged this

tension in her approach: “When sharing long-term information, companies need to

balance the benefits of disclosure with the risks of sharing competitive

insight. At GSK, we manage that tension by signaling key inflection points in

the business and sharing detail around those to build credibility for the

strategy.”

Others are worried about having their feet held to the fire if reality doesn’t

line up with the forecasted plan, particularly for reasons that are outside the

company’s control. While some of this is inevitable—and responding to events is

a reality—a well-communicated long-term roadmap typically includes a frank

discussion of the company’s assumptions and any risks that might upend them.

Investors informed by a long-term plan are prepared for a shift in guidance,

strategy, and performance when real-world conditions require a change from

initial plans. Indeed, this is an area where professional investors excel,

incorporating new information into their investment thesis and rapidly adjusting

to market change. In this way, long-term investors follow the example often

attributed to famed economist John Maynard Keynes: “When my information changes,

I change my mind. What do you do, sir?”

American multi-national chemical company Dow Chemical’s Vice President of

Investor Relations, Neal Sheorey, finds that his investors routinely assess how

future real-world conditions could impact his company’s performance. He tackles

the problem of forecasting conditions by providing a vision of what could be

possible based on historical market swings. In other words, rather than trying

to guess the future, he establishes scenarios based on past outcomes. This

provides a framework for investors to understand the inherent risks in the

company’s long-term strategy and to understand how performance will naturally

adjust if and when real-world conditions shift.

Some

points of resistance can even be turned into opportunities. Managers may be

concerned that discussing their company’s risks in a direct way may scare away

investors. But experience shows that long-term companies can use frank, balanced

conversations about risk as an opportunity to enhance investors’ understanding

of what goes into achieving the company’s strategic vision. They accomplish this

by discussing downsides and areas of potential upside. For example, Dave Huizing,

vice president of investor relations at Dutch health, nutrition, and materials

company DSM, uses his conversations about climate risk to highlight the

company’s sustainability mind-set. He emphasizes how DSM’s investments in

sustainability offer the company an attractive set of longer-term growth

opportunities while lowering their overall risk.

Long-term investors also have an important role to play. Too often, demands from

short-term investors or undue focus on short-term performance take center stage.

Why, companies ask, should they bother developing or disseminating long-term

plans or roadmaps when short-termism is so pervasive? The answer is that

investor surveys overwhelmingly indicate that money managers want long-term

information. Emerging evidence indicates that markets more broadly do react to

long-term plans. CECP, in conjunction with the research firm KKS Advisors,

analyzed the content of long-term plans shared by corporate managers at CECP’s

CEO Investor Forums, as well as the stock market reaction following these

presentations. Their research suggests that investors do trade on long-term

information: “The results show abnormal reactions for both stock prices and

trading volume for three and five days after the [long-term plan] presentation.

… The stock price and share turnover findings imply that the long-term plans

presented at the CEO Investor Forum contain information that investors find

relevant and meaningful [to their investment decisions].”

While

reorienting investor communications can sometimes seem like turning a

supertanker, change, once initiated, can happen quickly. Take the issuance of

guidance—forward-looking, numerical forecasts of a company’s anticipated

performance. Short-term quarterly earnings guidance peaked in popularity in

2003, when 75 percent of US firms issued quarterly forecasts. As the harm caused

by short-term guidance became better understood (described in our earlier work

Moving Beyond Quarterly Guidance: A Relic of the

Past), there was a significant reversal in trend—just 27.8

percent of S&P 500 companies gave quarterly earnings guidance in 2017.

The

same shift can happen for long-term guidance. On a global basis, long-term

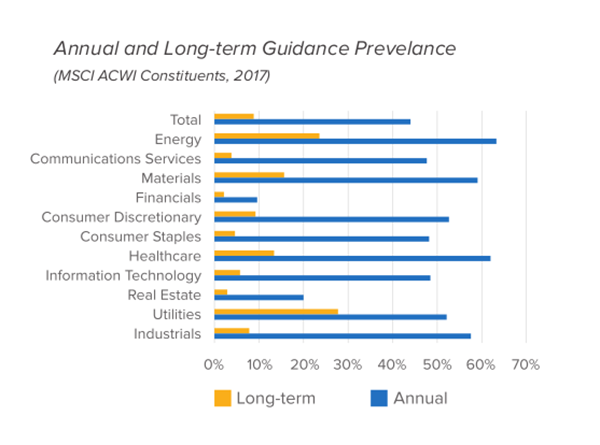

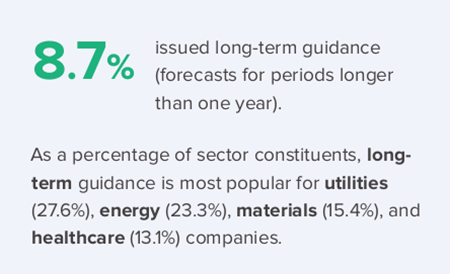

forecasts have a small following: 8.7 percent of MSCI All Country World Index (ACWI)

constituents issued longer-term guidance in 2017 (guidance for periods greater

than one year into the future), far fewer than the 44 percent of constituents

that issued annual guidance. If long-term investors spoke as loudly as their

shorter-term counterparts, these numbers could rapidly rise.

Rules of the Road: What Makes a Good Long-term Roadmap

Long-term roadmaps are about cutting through the short-term frenzy and focusing

on what matters. Companies that successfully implement long-term

communications—whether roadmaps alone or a full suite of long-term investor

communications approaches—focus on the information that really drives decision

making for long-term investors. In 2015, the Focusing Capital on the Long Term

initiative introduced a suggested framework for long-term investor

communications. The report,

Straight Talk for the Long Term,

highlighted 10 elements that institutional investors, corporate strategy

experts, and CEOs recommend companies include when formulating their long-term

communications plans. These 10 elements constitute a complete plan for long-term

investor communications. Collectively, they represent what investors view as the

“gold standard.”

Companies are typically comfortable with the first few elements. Expressing

their purpose, mission, and vision; explaining their business model and core

drivers of growth; and sharing management’s market view are all familiar talking

points for management teams in informal conversations. But taking the leap to

sharing a complete long-term plan in a formal way seems more challenging.

Discussing strategic goals, laying out a detailed execution plan, providing

metrics and targets that track strategic progress, and tying that progress to

capital allocation priorities and likely risks require careful consideration and

a coordinated approach.

Going

from zero to 10 is understandably daunting, but a long-term roadmap offers an

achievable first step. To help companies determine how best to start, FCLTGlobal

surveyed investment decision makers to identify their priorities for long-term

communication.

Although the overwhelming preference remains for a complete long-term plan,

respondents were in broad agreement that a good long-term roadmap lays out a

clear vision for the future based on the company’s competitive advantages and

core drivers of growth—the underlying determinants of a company’s success; it

then links these to long-term objectives and capital allocation priorities.

These elements, combined with a strategic plan to achieve those objectives and a

set of key performance indicators (and long-term guidance for them), constitute

the backbone of a good roadmap.

Many

leading global companies, including British energy firm BP, GSK, Japanese motor

manufacturer Nidec, North American home improvement retailer The Home Depot,

DSM, and British-Dutch transnational consumer goods company Unilever, have

adopted long-term roadmaps (or, in some cases, complete long-term plans) to aid

in their investor communications.

Their

examples demonstrate that the shift to long-term communications is achievable

and desirable, even for the largest, most scrutinized companies in markets

across the globe.

Companies that have implemented this approach find aligning investor

communications with long-term objectives allows them to speak to the horizon

that a majority of their investors find most relevant. But how can companies

best achieve that combination of information? As a start, they can think about

where the business is likely to be several years down the road. A good roadmap

explains how a company will get there and establishes specific, interim goals

that track the achievement of this vision. From there, they can elaborate on the

key elements identified as most important by long-term investors. These elements

include the following:

Competitive Advantages and Core Drivers of Growth:

These

can be identified by considering the questions: “At what do we excel?” or “What

differentiates us?” In the same vein, companies need to identify the sources of

current and future growth: “What will drive revenues in the future?” and “What

trends are we positioning the company to take advantage of?”

Some

companies include details on the competitive landscape, key customer segments,

primary technologies and products, and internal factors such as intangible

assets and organizational structure. Most investors suggest a focus on the input

factors (what drives the company and its strategy) and less attention on output

factors (what the earnings are now, next month, and next quarter).

Nidec

clearly defines management’s view of the four major core drivers of growth for

the motor manufacturing company: automotive electrification driven by a push for

decarbonization of the transportation sector; the expansion of robot

applications, particularly in the food, logistics, and service industries;

continued demand for power-saving motors for home appliances; and the rising

demand for further automation in the agriculture and logistics sectors, driven

by increasing labor constraints. These core drivers of growth are clearly linked

to the company’s five-year plan, and management offers an annual review and

update on how they see each developing.

Long-term Objectives:

A good roadmap provides a clear picture of where the company is going in the

next three to five years and beyond, including specific targets at both the

enterprise and business unit level. These objectives tend to include a mix of

operational and financial goals, as well as related assumptions.

|

When

companies present a vision for the future and discuss how they are positioning

the strategy to achieve that, this is the most believable sort of guidance. In

our view, a two- to three-year outlook tied to a longer-term vision is the gold

standard for investor communications.

– Felix Lanters, Head of Equities, PGGM |

For

example, to ensure simplicity and clarity, DSM focuses on two high-level,

long-term financial objectives: sharing target ranges for EBITDA (earnings

before interest, taxes, depreciation and amortization) and average, annually

adjusted net operating free cash flow. DSM’s investor relations team

communicates its value proposition, while also building credibility for the

strategy, by sharing a detailed annual Factbook that includes a review of past

performance against guidance metrics, segment milestones toward achieving group

targets, the details of key projects contributing to core growth initiatives,

and the company’s long-term objectives.

Strategic Plan:

In

our interviews with institutional investors, we found broad agreement that a

good roadmap also articulates the company’s high-level strategic plan and the

set of actions management plans to take to achieve their long-term objectives.

The strategic plan can also be used to frame discussions of critical risk

factors, both upside and downside, that could impact strategy, especially those

related to core business drivers. Using scenario analyses where appropriate can

also be helpful to illustrate risks and assumptions and explain forecast ranges.

Tata

Motors clearly lays out its business model and strategic priorities in its

roadmap, identifying long-term opportunities and listing key risks. The company

presents its strategic framework, detailing objectives by segment, as well as

segment-level key initiatives and actions taken, and spotlighting future areas

of focus for each segment. By highlighting risks alongside the business model,

the company elevates the risk conversation from one buried in legalese to one

related to business strategy, potential impacts, and mitigation tactics.

Capital Allocation Priorities:

Discussions of a company’s strategic plan go hand-in-hand with how the company

allocates capital (both its sources and its uses of cash). Laying out specific

capital allocation priorities lends credibility to the strategy and helps

illustrate how the company expects to finance its path forward. As GSK’s CEO

Emma Walmsley emphasizes, “Until you put the money where you say your strategy

is, it’s not your strategy.”

Many

companies have recognized the value of communicating their capital allocation

priorities to investors. In 2017, 21.8 percent of MSCI ACWI constituents offered

annual or longer capital expenditure (capex) guidance. Perhaps unsurprisingly,

companies in capital-intensive industries, or industries where investing in

long-lived assets or projects is common, tend to use capex guidance most

frequently. In 2017, 59.4 percent of ACWI energy sector companies, 38.8 percent

of materials companies, and 36.2 percent of utilities companies provided annual

or longer capex guidance.

The

Home Depot shares its planned approach to capital allocation with investors and

explains how this allocation supports its long-term objectives. Alongside its

strategic framework, the company issues three-year targets, updated annually and

rolled forward at periodic, company-hosted investor conferences (for example,

2018 targets were first introduced at its 2015 Investor Conference, while 2020

targets were first issued at the 2017 Investor Conference).

The

Home Depot’s capital allocation detail includes total forecasted spend, a

breakdown by spending category, and an outline of the return on invested capital

guidelines the company uses to inform its investment decisions—including its

target mix of debt to equity, targeted debt/EBITDAR (earnings before interest,

taxes, depreciation, amortization and restructuring) ratio, and benchmarking

criteria. Return of capital to shareholders is also included in the capital

allocation plan, highlighting the target payout ratio and preference for use of

cash to buy back shares only after meeting the needs of the business (and only

if the buybacks are deemed “value creating”).

Key Performance Indicators (KPIs):

Successful long-term roadmaps provide a mix of financial and operational metrics

(KPIs) tied to the company’s core drivers of growth. These metrics allow

investors to track progress toward long-term objectives and engage the executive

team in dialogue over their progress.

Metrics that help investors understand and follow the company’s progress over

time are the most helpful. These are typically metrics (1) that the company can

comfortably predict, (2) over which the company has a reasonable degree of

control, and (3) that are difficult for outsiders to estimate despite their

importance to the company’s strategy. Companies often contextualize these

metrics by connecting them to their long-term goals and by offering a three- to

five-year outlook for each (as a range, not a point estimate), as well as to key

risk factors and opportunities influencing that outlook. Further detail often

includes tying metrics to management incentives and capital allocation plans,

which can further help companies build credibility for their strategy among

investors.

As an

organization focused on developing long-horizon projects and assets, BP takes a

similarly long-view with investor communications. The company offers a five-year

plan for company performance, together with interim annual targets, and

regularly reports against 15 financial and operational KPIs. These KPIs are

shared with a five-year history for reference and include clear definitions for

how each metric is calculated, a brief discussion of the recent trend and any

relevant considerations, and information on how metrics are tied to compensation

plans.

BP

focuses its metrics and targets on things the company and its employees can

influence. Examples include their “Reserves Replacement Ratio,” which measures

the extent to which that year’s production has been replaced by new proven

reserves added to the reserve base, and their “Underlying Replacement Cost

Profit,” which measures the replacement cost of inventories sold in the period.

By using a mix of operational and financial targets, BP makes it easy to track

progress toward long-term objectives while stripping out the “noise” caused by

factors outside the company’s control.

|

Identifying Appropriate Metrics

Which

metrics belong in a company’s roadmap? Investor relations professionals have

found it’s important to monitor those that both management and investors

consider most important to valuing and evaluating a company. Here are some

ideas:

-

Get a sense of

commonly used industry metrics by surveying peers and competitors.

-

Ask long-term

investors which metrics they find most helpful.

-

Consider the

relevance of a company’s internal metrics for external stakeholders. If it’s

important enough to be used as a yardstick for business success, then odds are

it should be on the short list of metrics to be publicly shared, particularly

if it’s tied to incentive compensation.

-

A number of

organizations, including the Sustainability Accounting Standards Board, and

the International Integrated Reporting Council offer various frameworks and

metrics for disclosure which can link to long-term roadmaps.

|

Research by Alex Edmans, Mirko Heinle, and Chong Huang offers cautionary

evidence to keep in mind when selecting metrics. The authors demonstrate that as

long as stock markets better incorporate “hard” information than “soft,”

disclosing more hard information will skew managers’ real decisions toward

improving hard performance measures (such as improving earnings) at the expense

of soft performance measures (such as intangible investments).

While

the study focuses on the impact of an increase in reporting frequency, this

finding is instructive for forming long-term roadmaps as well. Long-term targets

could lead to excessive management of those targets, so that companies sharing

KPIs could consider including a balanced mix of both financial (“hard”) and

operational (“soft”) metrics as targets. This mix makes it less likely that

managers will game one metric over another and will ensure their focus remains

on achieving both.

Hitting the Road: Developing and Putting a Long-term Roadmap into Practice

Effectively delivering a long-term roadmap to the market requires companies to

lay critical groundwork, both internally and externally. Investor relations

professionals interviewed for this project emphasized that roadmaps require

internal buy-in and willpower to stick to this approach. For example, for the

past 10 years, DSM has prioritized sustainability as its key business driver.

The combination of the shifting business portfolio and DSM’s

sustainability-based growth initiatives required investors to understand the

long-term plan and appreciate the company’s strategic investment goals. To

achieve that understanding, the investor relations and corporate communications

departments worked with the board, CEO, and CFO to develop a unified

communications strategy focused on the long-term storyline, as well as

developing stakeholder buy-in for the long-term strategy. Similarly, GSK’s

launch of its long-term roadmap followed months of work, which included

collecting feedback from numerous stakeholders, both internal and external.

In

constructing a long-term roadmap, it helps to keep things simple. Unilever CEO

Paul Polman’s concluding remarks at the company’s 2017 Investor Event consisted

of only seven slides. Starting with reviewing the company’s strengths, he then

summarized how Unilever would build on these strengths to drive the next phase

of growth; laid out specific short-, medium-, and long-term priorities;

highlighted potential sources of risk; and closed by reconfirming the company’s

outlook targets.

Once

the roadmap has been developed internally, it’s time to take it on the road.

Investors suggest that companies consider launching the plan at a high-profile

event, such as an annual meeting, capital markets, or investor day. In fact, 79

percent of the investors we surveyed identified a company-hosted investor or

capital markets day as the best venue for sharing a long-term plan or roadmap.

Post-launch, management and investor relations professionals start every

conversation, including those with the sell side and the media, by reminding

their audience of the company’s long-term goals. Companies have also found it

valuable to provide investors with exposure to wider senior management, beyond

just the CEO or CFO. Demonstrating depth of leadership, backed up by unified

messaging, makes investors comfortable that the whole team is on board with the

long-term plan and working together to execute it. Finally, companies find being

clear about how and when the roadmap will be updated helps investors anticipate

the communication cadence. On that question, investors were clear: they prefer

annual updates by a significant margin.

Getting to the Destination

Long-term roadmaps offer a potential bulwark against short-term pressures. In

our study, 100 percent of investors said they either always or occasionally

encourage companies to share their long-term plans.39 More than 86 percent of

investment decision makers say they want metrics oriented toward expected

performance at least three years out. Success stories show that the hurdles to

adopting long-term investor communications can be overcome.

A

long-term roadmap is a manageable first step toward building a complete

long-term communications strategy. By sharing core drivers of growth,

competitive advantages, long-term objectives, and the company’s strategic plan

(including capital allocation priorities and interim targets), companies can

provide investors with the information they need without getting caught in the

frenzy of quarterly targets. Investment decision makers have made it clear what

they want: a long-term roadmap to provide a unifying framework and vehicle to

communicate.

By

transitioning to long-term roadmaps, companies can begin to build the

communications foundation for what really matters: creating long-term,

sustainable value.

The

complete publication, including footnotes and appendix, is available

here.

|

Harvard Law School Forum

on Corporate Governance and Financial Regulation

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2019 The President and

Fellows of Harvard College. |