Business Day

Valeant’s

High-Price Drug Strategy

OCT.

2, 2015

|

The headquarters of Valeant

Pharmaceuticals International, a multinational specialty drug

company based in Quebec.

Christinne Muschi/Reuters

|

Talk

about a reversal of fortune.

Until

recently, investors were positively star-struck by drug companies that

could raise prices indiscriminately, letting their patients struggle

to pay the freight. Lauded for a laserlike focus on shareholder

returns, companies like

Valeant Pharmaceuticals International,

a multinational specialty drug company based in Quebec, received high

marks and even higher valuations from besotted shareholders.

| |

Fair Game

A

column from Gretchen Morgenson examining the world of finance

and its impact on investors, workers and families

See More »

|

| |

|

Now,

however, investors are beginning to see the peril in such a business

model. Sure, price jumps may generate earnings and stock gains, but

when the enrichment of a few comes at the cost of many, unwanted

scrutiny often follows.

Hijacked drug prices blasted to the forefront two weeks ago after a

report in The New York Times

told the story of how Martin

Shkreli, the chief executive of the privately held Turing

Pharmaceuticals, bought Daraprim, a 62-year-old infectious disease

drug, and immediately raised its price to $750 from $13.50 a tablet.

When a

firestorm ensued, Mr. Shkreli accurately noted that his was not the

only company to acquire a drug and then send its price into the

stratosphere.

The

spotlight soon fell on Valeant, which generated $8.25 billion in

revenue last year, up 43 percent from 2013. Among its well-known drugs

is Ativan, a treatment for anxiety.

Valeant caught the eye of Congress this year after it increased the

price of two heart medications it had just bought the rights to sell:

Nitropress and Isuprel. Valeant raised the price of Nitropress 212

percent and Isuprel 525 percent.

Democratic members of the House Committee on Oversight and Government

Reform, led by Elijah Cummings, the Maryland Democrat who is its

ranking member, have been investigating rocketing drug prices. This

year

they asked Valeant to provide

documents about the increases; it declined.

So

last Monday, 18 Democratic members of the committee asked its chairman

to

subpoena Valeant for those

documents.

It is

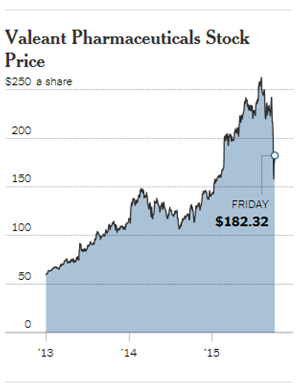

unclear whether the subpoena will be issued. But Valeant’s stock slid

16.5 percent on the news. It recovered somewhat later in the week, but

it has lost more than 30 percent since its August high closing price

of $262.52.

With

the stock plummeting, J. Michael Pearson, Valeant’s chief executive,

sent

a letter to reassure employees.

In it, he rejected investor concerns that the company’s strategy

relied on big price increases. He noted that half of the company’s

sales came from domestic and international businesses in which it had

realized small or no net price increases.

Valeant is “committed to focusing on our key stakeholders while

delivering consistently high performance,” its

website states.

But

satisfying customers’ needs for affordable drugs can conflict with

company executives’ desires for a rising stock price. At Valeant,

executive pay is heavily tied to

shareholder returns.

Laurie

Little, a spokeswoman for Valeant, responded in a statement that the

company priced its treatments based on many factors, “including

clinical benefits and the value they bring to patients, physicians,

payers and society.” It also has “robust patient assistance programs

to help patients who face financial obstacles,” she said.

One

argument for high prices on

pharmaceuticals is that the money

goes to research for new cures. But this is not a Valeant strategy.

While

other multinational pharmaceutical companies spend well into the

double digits as a percentage of sales, Valeant’s 2014 annual report

shows that the company spent $246 million on research and development

— just 3 percent of sales. Another way to think about that: Valeant

paid its five highest-paid executives 1.5 percent of sales, or $123

million, last year.

On the

question of research, Valeant’s spokeswoman said in a statement that

the company “measures its success on output (i.e., results) rather

than input (i.e., spending).”

Valeant’s History of Deal Making

The drug company is known for

growing through acquisitions and cutting costs.

-

BIOVAIL

The drug company was created in a merger of Biovail of Canada

and a predecessor company based in Aliso Viejo, Calif.

(2010)

-

CEPHALON

The biopharmaceutical company

rejected a bid from Valeant

as opportunistic and too low. (2011)

-

MEDICIS

Valeant agreed to buy the dermatological drug company for

about $2.6 billion. (2012)

-

ACTAVIS

Merger talks fell through after a number of concerns from the

target company’s directors, including the size of the deal

premium. (2013)

-

BAUSCH & LOMB

The eye care company sold itself for about $8.7 billion,

sidestepping an I.P.O. (2013)

-

ALLERGAN

The company, maker of Botox, rejected an

unusual hostile bid from

Valeant and a hedge fund. Valeant was

criticized in the

bitter takeover battle

for

cutting R.&D. (2014)

-

SALIX

Faced with the prospect of letting another deal slip through

its fingers, Valeant substantially raised its bid, putting a

quick end to a bidding war. (March 2015)

-

SPROUT

Two days after winning regulatory approval for the first pill

to aid a woman’s sex drive, the company was acquired.

(August 2015)

|

|

Rather

than developing drugs, though, Valeant acquires them. Since 2010, it

has acquired companies with a total value of at least $36 billion,

mostly in the United States. It is the sixth-largest acquirer,

globally, by deal size.

In

2010, the predecessor to Valeant, based in California, was acquired by

Biovail, a Canadian company. It relocated to Canada, a jurisdiction

with a lower tax rate; the combined operations were named Valeant.

The

move to Canada has been highly beneficial to Valeant, as detailed in a

recent congressional

report on the impact of the

United States tax code on corporate activities. Published in July by

the Senate Permanent Subcommittee on Investigations, the report found

that by moving to Canada, Valeant lowered its statutory tax rate to 27

percent from 35 percent.

But

that barely captures the true scope of Valeant’s ability to escape

taxes. Its actual cash tax rate is far lower, the report found.

Valeant’s effective cash tax rate has fallen substantially, too, to

3.3 percent last year from 5.9 percent in 2010.

This

rock-bottom tax rate turbocharged the company’s expansion by

acquisition, according to Howard B. Schiller, a Valeant director and

its former chief financial officer. He told Senate investigators,

“There is no question that we would not be in the same place we are in

today if we had a higher tax rate.”

Valeant’s acquisitions have clearly generated wealth for its

shareholders. The same cannot be said for many of the workers at the

companies it acquired.

The

Senate report details layoffs made by Valeant after three large

acquisitions: Medicis Pharmaceutical in 2012, Bausch & Lomb in 2013

and Salix Pharmaceuticals this year.

When

Medicis was acquired, it had 790 full-time employees, the report said.

Valeant terminated 750 of them, mostly in the United States.

Bausch

& Lomb had 4,103 workers when Valeant came calling. It fired 3,000

workers in that acquisition, half domestically.

As for

Salix’s 977 workers, Valeant is planning to jettison 420 of them, all

based in America. The company has also said it will transfer some of

Salix’s contract manufacturing to Canada and Britain from the United

States.

As of

June, Valeant’s full-time American work force was 5,725, the report

said. Its overseas head count was 13,644.

Valeant is by no means the only company whose strategy skews rewards

to executives and shareholders. That’s unfortunately the way the game

is played nowadays.

But

does it have to be? A company’s earnings are not generated in a

vacuum. They are a byproduct of its practices and principles. If

investors assessed corporate earnings quality through that kind of

lens, they might just help make the world a better place.

Crazy,

I know. But isn’t it even crazier to leave everything up to executives

who manage only to their stock price?

A version of this article appears in print on October 4, 2015, on page

BU1 of the New York edition with the headline: Side Effects of

Hijacking Drug Prices.

© 2015 The

New York Times Company