|

Editor’s Note:

Ali Saribas is

a Partner at AQTION. This post is based on his AQTION study. |

AQTION, leveraging its proprietary database powered by SquareWell

Partners, published its second review on how the world’s largest 65

investors (hereafter referred to as the “Top 65”) are evaluating

governance and sustainability issues and stewarding their portfolios.

Together these investors (including some of the largest Assets

Managers, Sovereign Wealth Funds, and Pension Funds) have nearly

USD 91 trillion in Assets Under Management (AUM). See a summary

post of the findings from last year’s study.

In this year’s analysis of the Top 65, the composition of the universe

remains almost identical with the previous year, with only one change:

Voya Investment Management (Asset Manager, US) replacing Baillie

Gifford (Asset Manager, UK). To maintain comparability, the study

retained the same factors used in the previous year’s assessment,

while also incorporating new factors designed to capture investor

sentiment on emerging topics of interest, such as artificial

intelligence.

Notably, this year’s analysis looked athow these influential

investors voted on high-profile situations. This includes, for

example, the 2024 board contest at Walt Disney and the controversial

approval of Elon Musk’s multi-billion dollar pay package at Tesla.

These real-world examples offer valuable context to understand how the

Top 65 investors are exercising their influence on critical corporate

governance matters.

The full report is available here.

Below, we highlight some of the key takeaways from AQTION’s review of

the stewardship activities of the Top 65 investors, with selected

points explored in greater depth.

i. Stewardship Teams

Implementation of structures necessary for stewardship activities –

such as the introduction of a stewardship team, or publication of a

voting policy – are mature in their development.

Regulatory turbulence, especially SEC’s revised guidance for a more

stringent approach to monitoring investor activities that could

influence corporate control, may lead investors to carefully evaluate

their engagement strategies with portfolio companies and be less

transparent in engagements, leaving companies to rely more heavily

on their public positions and voting behavior to understand their

position.

ii. Pass-Through Voting

As Pass-Through Voting proliferates among index investors, such

as BlackRock and Vanguard, active managers remain reluctant to adopt,

indicating that voting is more strongly regarded as necessary for

active fund management.

iii. Voting Guidelines

Only 18 investors have published one or several regional policies,

indicating that stewardship is generally configured to apply global

principles. Notably, State Street Global Advisors consolidated

several policies into one global position in 2024.

Investors’ voting guidelines published in 2025 have also generally

become less prescriptive and more principles-based compared to

previous iterations. Notably, several investors have scaled back their

focus on Diversity, Equity & Inclusion (DEI) issues in response to

recent political backlash, particularly in the U.S. However, no

similar shift has been observed regarding climate-related

expectations, which remain an important issue for investors.

iv. Proxy Advisors

Proxy Advisors continue to be influential on investor vote decision

making, but are not commonly relied on heavily. ISS continues to be

the clear leader in supplying research, however, Schroders

switched to Glass Lewis as their primary proxy advisor in the year.

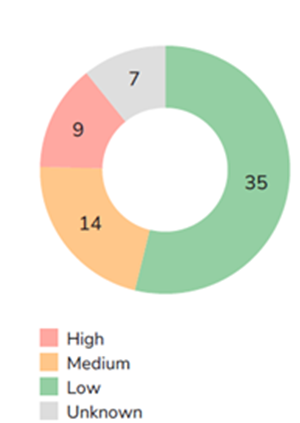

While many investors seek recommendations from Proxy Advisors, most

of the Top 65 investors have developed their own internal voting

guidelines. To this end, AQTION notes that only 9 of these

investors exhibit a “High” reliance on their chosen Proxy Advisor’s

recommendations, whereas 35 investors show a “Low” reliance (see

Graph 1). As highlighted by ISS’s latest Best

Practices Principle Statement, approximately 91% of the

total voted shares processed by ISS on behalf of their clients are

linked to clients’ custom voting policies. This means that

rather than relying on ISS’s standard research recommendations,

investors have ISS apply their own voting guidelines when determining

how to vote at general meetings.

Graph 1 – Investors’ Reliance on Proxy Advisor Recommendations

v. Stewardship Transparency – Votes and Rationales

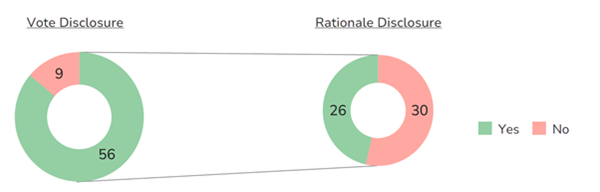

Investor Voting Behavior and Rationale: 56 of the Top 65 investors

disclose their voting records, with close to half providing vote

rationales (see Graph 2). A

few, such as CalPERS and Norges Bank Investment Management (“NBIM”),

go further by pre-declaring their voting intentions, while others like

Legal & General Investment Management (“LGIM”) and Neuberger Berman do

so only for high-profile or contentious votes.

Graph 2 – Investors’ Vote and Rationale Disclosure Practices

vi. Investor Communication on Key Topics

Despite ongoing pushback against elements of the ESG ecosystem in

2024—including the withdrawal of several prominent investors from

Climate Action 100+ and the suspension of the Net Zero Asset Managers

Initiative in January 2025, investors continue to communicate their

expectations on a broad spectrum of topics ranging from executive

pay to biodiversity.

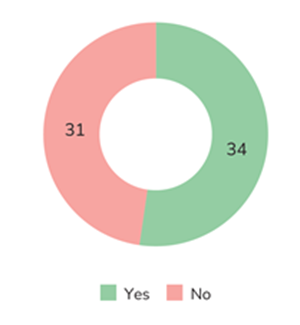

vi.a. One-Off Awards

Investors generally have reservations about awards granted outside

of the standard pay package (“One-Off Awards”), considering these

awards often reward executives for actions widely considered to be

within the scope of their responsibilities. AQTION finds that 34

out of the Top 65 investors provide insight into this topic (see Graph

3). While 8 investors, such as J.P. Morgan Asset Management

(“JPMAM”) and Aberdeen Investments are against one-off awards as a

matter of principle, other investors (26 of the Top 65) may support

special awards outside of Remuneration Policy where the company can

demonstrate truly exceptional circumstances and/or significant

additional value creation.

Graph 3 – Investors That Have Guidelines on One-Off Awards

vi.b. Artificial Intelligence

As Artificial Intelligence (“AI”) rapidly transforms industries

and business models, investor scrutiny on its ethical use, governance,

and long-term impact has intensified. AQTION finds that 26 of the

Top 65 investors have published dedicated position papers on AI,

outlining their expectations for how companies should responsibly

integrate AI into their operations. These papers emphasis the need

for clear governance frameworks, transparency in AI development and

deployment, and an understanding of the societal and ethical risks

involved. Investors are urging companies to demonstrate

accountability, ensure fairness, and safeguard against potential

negative consequences as AI becomes a more integral part of business

strategies.

vii. Shareholder Activism

Shareholder Activism:

Activism is now a core component of voting guidelines, with 39 of

the Top 65 investors incorporating criteria for evaluating activism

situations. This marks a broader shift toward proactive

stewardship, as traditional investors increasingly use public

channels—such as press releases and media statements—to hold companies

accountable. Notably, 29 investors have recently disclosed concerns

about portfolio company performance or governance in case studies and

stewardship reports. In 2024 and early 2025, Neuberger Berman

exemplified this trend by publishing detailed voting rationales for

high-profile activism cases, including Walt Disney (US), Keisei

Electric Railway (JP), UGI Corporation (US), and Rio Tinto (UK, as

well as for uncontested votes.

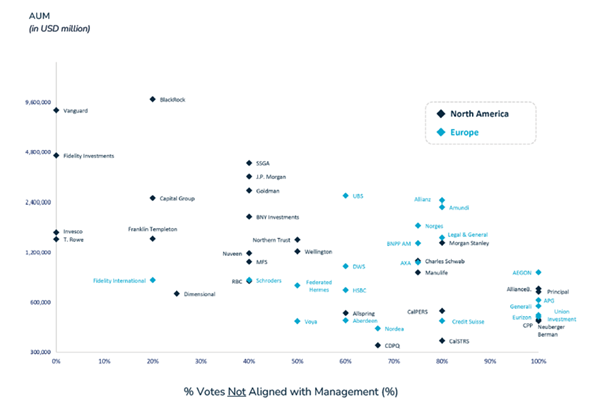

viii. Investors’ Voting Scorecard

AQTION’s analysis of the Top 65 investors voting behavior suggests

that European asset managers appear more comfortable challenging

management through their votes, while U.S. investors show a marked

hesitance to do so (see Graph 4). This divergence is particularly

evident in high-profile cases involving companies such as Boeing,

Apple, ExxonMobil, and Walt Disney.

Graph 4 – Investor Voting Patterns in High-Profile Shareholder

Meetings

|

Harvard Law School Forum on

Corporate Governance

All copyright and trademarks in

content on this site are owned by their respective owners. Other

content © 2025 The President and Fellows of Harvard College.

Privacy

Policy |