A new marketplace is letting investors sell their votes. Not everyone

is happy about it.

Shareholder Vote Exchange is a small California-based startup that

runs auctions for the rights to vote in shareholder meetings. Backers

say it can help ordinary investors get cash for voting rights they are

unlikely to use. Critics worry that buying and selling shareholder

votes is rife with the potential for abuse.

Here is how it works. Suppose you are an investor with shares of

Walgreens Boots Alliance, but you

are not interested in participating in the company’s annual meeting on

Thursday. If you are registered with Shareholder Vote Exchange’s

website, you can sell the proxy voting rights—which were recently

trading at 1 cent per share—for that meeting.

The buyer can use your proxy to vote on agenda items at the Walgreens

meeting—for instance, the board election, or a proposal by a group

of nuns that would require the drugstore giant to report on

the disposal of cigarette waste. You remain the holder of the shares.

The next time Walgreens has an annual meeting, you can vote your

shares as usual or sell your proxy voting rights again.

Effectively, selling votes is a way for investors to earn additional

yield from an asset that often goes untapped, said Andrew Shapiro, a

board adviser to Shareholder Vote Exchange. Only about 30% of shares

held by individual investors are used to vote, according to

financial-technology firm

Broadridge Financial Solutions.

“Many retail investors throw their votes away because they don’t want

to read the proxy or because they feel their votes don’t matter,” said

Shapiro, the managing member of Lawndale Capital Management, an

activist fund manager.

Casual observers might be surprised that it is legal to buy and sell

shareholder votes. After all, it is against federal and state law to

buy votes in political elections.

|

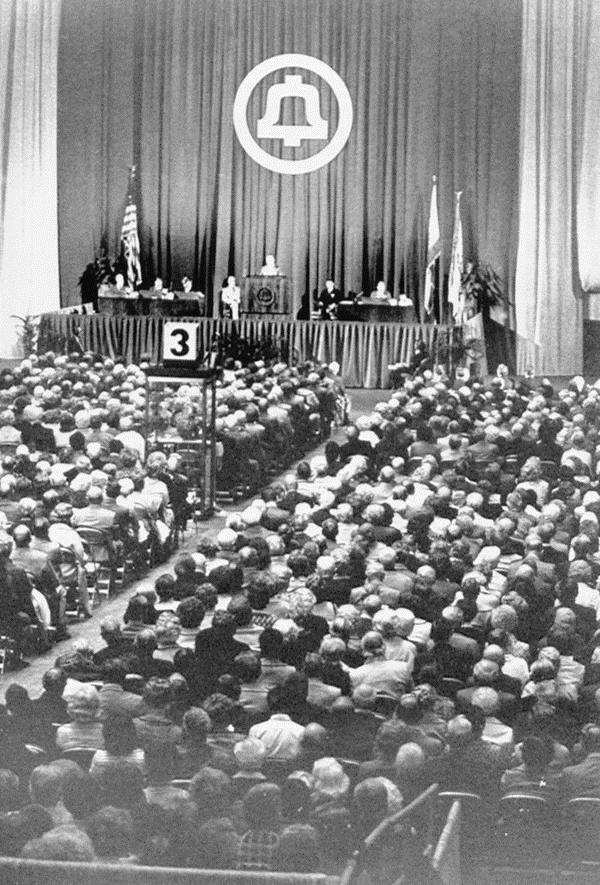

Billions

of votes are cast in U.S. corporate meetings annually.

Above, an AT&T shareholder meeting in the 1970s. . PHOTO: BETTMANN

ARCHIVE Billions

of votes are cast in U.S. corporate meetings annually.

Above, an AT&T shareholder meeting in the 1970s. . PHOTO: BETTMANN

ARCHIVE

|

But lawyers say that in most U.S. states—and notably in Delaware,

where most large companies are incorporated—it is legal for

shareholders to sell their votes in corporate elections.

The catch is that the buyers of those votes could run into trouble,

especially if they are the companies themselves. For instance, if a

company purchased votes to block a takeover attempt that its board and

management didn’t like, it could be hit with lawsuits arguing that

executives failed to act in shareholders’ best interests.

In a 1982 ruling, the Delaware Court of Chancery dismissed the

argument that vote buying was inherently illegal, calling it an

outmoded idea. But the court also warned that the practice was “easily

susceptible of abuse” and said specific instances of vote buying could

be scrutinized for fraud or efforts to disenfranchise

shareholders.

Business leaders, regulators and academics have debated the ethics of

buying shareholder votes for decades. Some have argued that creating a

market for proxy votes would enhance shareholder

democracy and ultimately make companies better-run. Others

say it is risky to decouple the right to vote from ownership of the

shares because the votes could end up in the hands of someone who

doesn’t want the company to succeed.

Shareholder Vote Exchange has some safeguards. It requires buyers to

attest that they have a net long position in a company’s stock—so for

instance, a short seller betting against the stock couldn’t buy votes,

according to Preston Yadegar, the startup’s CEO and founder.

“There are a lot of different ways this could be misused,” he said.

“If we are smart and proactive in thinking about those scenarios, we

can mitigate or entirely prevent them.”

Still, there is potential for abuse, said Henry Hu, a law professor at

the University of Texas at Austin. Hu outlined a scenario in which an

investor owned shares in two companies, one of which was set to

acquire the other for a lofty price. If the investor had a large stake

in the acquisition target, he might buy votes to ensure the deal goes

through, even if it is a bad deal for the acquiring company.

“Not all vote-buying is bad,” Hu said. “But if the buyer of the votes

has an overall negative economic interest in the company, that can

lead to value-destructive results.”

Yadegar, who is 25 years old, started Shareholder Vote Exchange in

2021, the year after he graduated from Boston University with a

bachelor’s degree in computer science and philosophy. The startup has

been funded by Yadegar’s family and friends, but he said talks are

under way with potential strategic and financial investors.

So far, about 200,000 proxy votes—a tiny slice of the billions of

votes cast in U.S. corporate meetings annually—have been traded on

Shareholder Vote Exchange. Yadegar expects volumes to grow with the

2024 proxy

season—the period each spring when many companies hold

votes on board composition and other corporate-governance matters.

One potential growth area for Shareholder Vote Exchange, Yadegar said,

is helping companies achieve the quorum needed to approve deals or

measures such as stock splits. Since the Covid-19 pandemic, meeting

quorum requirements has

proven to be difficult for companies with a large

proportion of shares held by individual investors, such as

AMC Entertainment Holdings.

Market veterans had mixed views on Shareholder Vote Exchange’s

prospects. Some predicted that institutional investors would stay away

because of perceptions of vote buying as disreputable. Others said it

was inevitable that such a market would emerge.

“Wall Street is famous for taking investments apart into little

pieces,” said Sarah Teslik, president of VMI, an investor and

governance advisory firm. “It’s not surprising that someone has

created a platform that lets you sell the vote if it doesn’t interest

you.”

Write to Alexander Osipovich at alexo@wsj.com