|

SEMAFOR

Liz Hoffman |

|

A win for

corporate raiders

Updated Jan 3, 2023, 1:26pm EST

※ THE

SCOOP

U.S. rules

governing how activist hedge funds and hostile bidders can accumulate

stock positions in secret haven’t been meaningfully changed since

1968.

Now, the

Securities and Exchange Commission is finalizing reforms and likely to

back off its most far-reaching proposals, people familiar with the

matter said. That retreat would hand a win to investors like Bill

Ackman and Carl Icahn, and their brokers on Wall Street.

|

Getty

Images/Sylvain Gaboury |

At issue are rules

on when and how investors have to disclose stakes of at least 5%,

which have been used to push for changes at some of America’s

corporate giants. The agency’s proposal to narrow the deadline for

investors to publicly report their stake, from 10 days to five, is

likely to survive in the final measures, people familiar with the

matter said.

But two other

major rule revisions the SEC proposed in March are likely to be

abandoned or significantly pared back after feedback from market

players.

One would sweep

stock contracts with Wall Street banks – which mimic exposure to stock

ownership but don’t carry the right to buy the underlying shares –

into an investors’ stake for purposes of calculating the 5% trigger.

That proposal would also rope those banks into a hedge fund’s camp for

purposes of determining whether an investor “group” had been formed.

This fall, the two

camps made their case directly to the SEC, people familiar with the

matter said. Wachtell, Lipton, the staunchly pro-management law firm,

sent two heavyweight lawyers, David Katz and Leo Strine, to lobby the

SEC for tighter rules. Stephen Fraidin of Cadwalader, Wickersham &

Taft LLP and Berkeley Law’s Frank Partnoy went to argue the case of

activists.

No decisions have

been made, and the SEC could choose to re-propose preliminary rules

for a new round of comments from the public. A final rule is expected

sometime this summer, the people said.

☼ LIZ'S

VIEW

The

investing world moves faster than it did in 1968, and the speed with

which market information moves means the SEC can tighten the 10-day

window and still keep the balance between investors, who need an

incentive to make bold bets, and the rights of corporate managers they

target not to be blindsided.

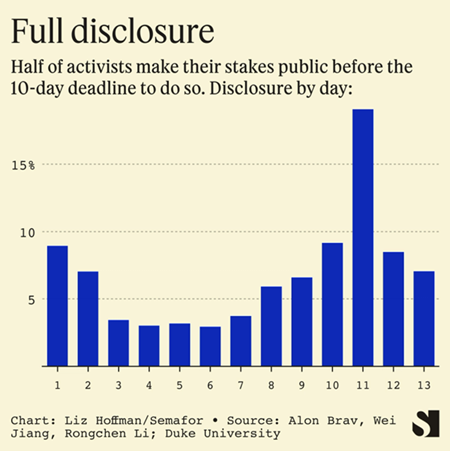

Most activists don’t even use the full 10 days to build their stakes.

Even one of the biggest activist hedge funds, Elliott, isn’t

opposing that move.

But

the SEC’s other proposals would hamstring activists’ ability to use

common trading strategies, like swaps, that boost their economics but

not their strongarm power. And they would make it impossible for most

banks to work with activists, who can play constructive roles in

shaking up entrenched management or calling out poor performance.

Take the swaps rule. Hedge funds use swaps contracts, which are

cheaper than outright share purchases, to boost their economic

ownership in companies but don’t give an activist any additional

votes. The contracts require investment banks to deliver the cash

value of the stock in the future, so they go out and buy the

underlying shares. The SEC’s proposal would include those swaps in

the investor’s position for purposes of triggering the 5% threshold.

The

proposed rule would also require that a bank disclose every

transaction it made in the shares in issue – an insane requirement for

a large Wall Street brokerage desk, which might trade thousands of

individual stocks in any given day.

And

if the SEC really wants to breathe some life back into the 13D rules,

it could start by sanctioning Elon Musk for flagrantly violating them

in his pursuit last spring of Twitter. He blew the filing deadline; trading

records show he owned 5% of the company by March 14, but he

didn’t make his first filing until three weeks later.

And

even then, he disclosed his stake on a form reserved

for passive investors who don’t plan to seek control of the company or

influence its board. By that point, Musk had unleashed a string of

tweets criticizing the company’s management and had talked

to Twitter about joining its board for weeks.

▒ ROOM

FOR DISAGREEMENT

Supporters of the

rule argue the swaps market does need more transparency, and cite the

swift collapse in 2021 of Archegos Capital Management. The fund had

built up huge positions in Viacom, Shopify and other stocks through

shadowy swaps trades, in some cases equivalent to 50% or more of the

float – all without having to make so much as a single disclosure.

When the stocks

fell, it started a swift collapse that ultimately cost the banks

Archegos was doing business with $10 billion. “This combination of

leverage and anonymity proved devastating,” Wall Street nonprofit

watchdog Better Markets wrote to the SEC in support of the changes.

Six Democratic

senators, including Elizabeth Warren and Sherrod Brown, have made the

same point. They argue the changes are needed “to ensure that [swaps]

are not used to hide a stake in [a] public company or a large position

that could destabilize financial markets.”

◙ NOTABLE

-

WSJ on how Archegos’ blow-up renewed

calls for more transparency in swaps. “The private

marketplace was not aware of the extent of the risk exposure,

because it did not have enough information,” one expert told the

paper. “The antidote for that is more disclosure.”

-

A paper commissioned

by a group of investors dove back into the congressional record to

untangle the origins of the Williams Act, and argues that no reforms

are needed.

© 2023 SEMAFOR INC. |