The term ESG is less than two decades old, but it may already be

coming to the end of its useful life.

The acronym dates back to 2004, when a report commissioned by the UN

called for “better inclusion of environmental, social and corporate

governance (ESG) factors in investment decisions”. In the wake of

corporate scandals such as Enron and WorldCom, and the Exxon Valdez

oil spill, financial institutions eagerly signed on to the “global

compact”.

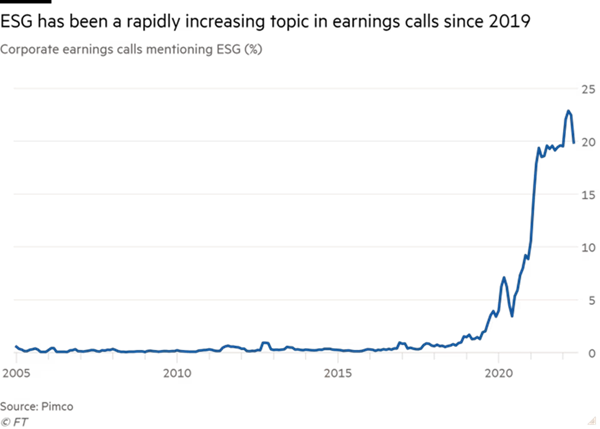

It took a while to catch on. Between May 2005 and May 2018, ESG was

mentioned in fewer than 1 per cent of earnings calls, according to

analysis by asset manager Pimco. But once ESG became mainstream, it

quickly became ubiquitous in the corporate landscape. By May 2021 it

was mentioned in almost a fifth of earnings calls, after a surge in

prominence over the pandemic.

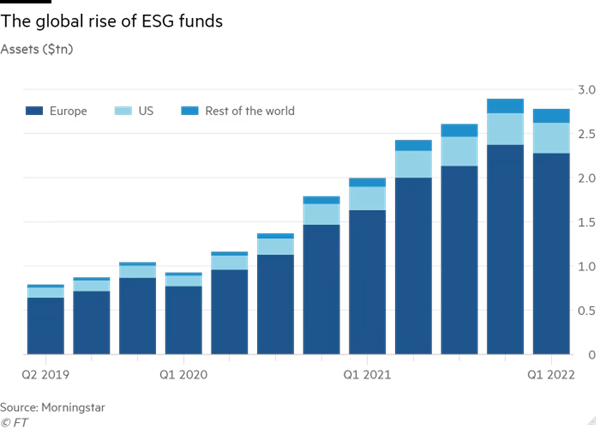

Investing within an ESG framework is now the fastest-growing segment

of the asset management industry. Assets in ESG funds grew 53 per cent

year on year to $2.7tn in 2021, according to data provider

Morningstar, amid a gold rush by asset managers to tap into rising

investor demand by rebranding their funds as sustainable or launching

new ones.

The term has become an increasingly broad catch-all for a range of

approaches to investment: everything from negative screening (removing

sectors such as tobacco or defence) to positive screening (picking

sectors such as clean energy), to really any kind of strategy that

promises to bring about positive social or environmental change.

This flexibility can be a positive thing, allowing such funds to

“collectively appeal to a broad range of investors and stakeholders”,

wrote Elizabeth Pollman, a professor at the University of Pennsylvania

Carey Law School, in a paper titled

The Origins and Consequences of

the ESG Moniker.

But there’s a fine line between flexibility and ambiguity, and ESG’s

critics say some companies and investors are using the loosely defined

term to “greenwash,” or make unrealistic or misleading claims,

especially about their environmental credentials.

Those criticisms came into sharp focus on May 31, when German police

raided the offices of asset manager DWS and its majority owner

Deutsche Bank as part of a probe into allegations of greenwashing. It

was the first time that an asset manager has been raided in an ESG

investigation and signals a moment of reckoning for the industry.

It’s a “real wake-up call,” says Desiree Fixler, the former DWS

executive who blew the whistle on her company for allegedly making

misleading statements about ESG investing in its 2020 annual report (DWS

denies wrongdoing). “I still believe in sustainable investing, but the

bureaucrats and marketers took over ESG and now it’s been diluted to a

state of meaninglessness,” she says.

On top of the allegations of greenwashing at the industry’s highest

levels, there is the impact of Russia’s invasion of Ukraine, which is

forcing companies, investors and governments to wrestle with

developments that at times appear to pit the E, the S and the G

against one another. For example, governments in Europe are reneging

on environmental goals by turning to fossil fuels to reduce dependence

on Russian gas, in order to fulfil ethical goals.

“The war in Ukraine is an incredible challenge for the world of ESG,”

says Hubert Keller, managing partner at Lombard Odier. “This conflict

is forcing the questions: what is ESG investing? Does it really work?

And can we afford it?”

Some people wonder whether the term still has any meaning at all. “The

acronym ESG is a bit of a confused compact because it muddies at least

two things,” says Ian Simm, founder and chief executive of £37bn asset

manager Impax Asset Management, a pioneer in sustainable development.

“One is an objective assessment, around risk and opportunity. And the

other is around values or ethics. And so people get themselves tied in

knots because they’re not really clear about what exactly ESG

investing is about.”

Simm is among those investors who believe that while there have been

huge benefits that have arisen from bundling together ESG — notably

waking up the world to thinking about issues as varied as climate

change, gender diversity and the impact of corporations on communities

— the term has, in effect, come to mean all things to all people, and

might be nearing retirement.

“I think we should dial down or even stop using the phrase ESG,” says

Simm. “We should push very hard for people to be clear about what they

want when they use it. And in an ideal world, ESG would disappear as

an acronym . . . and we would find a better way of labelling the

conversation.”

The fog of war

If this is a transformational moment for the investment landscape,

some say it is also an opportunity to redefine what it means to invest

sustainably.

The war in Ukraine ought to be considered “an evolution for ESG rather

than muddying the waters”, says Sonja Laud, chief investment officer

at Legal and General Investment Management. “It might not be the last

time we have to reconsider the framework of what makes a sustainable

investment.”

She points to three core areas — defence, energy and sovereign risk —

where the shift has been most pronounced. “These are not new topics

but they have been put into the spotlight because of these events.”

Defence presents one of the most immediate challenges. For years, many

banks and investors across Europe have refused to back defence

companies, as it goes against their ESG policies. Among them was

Sweden’s SEB bank, which unveiled a new sustainability policy last

year that included a blanket ban on any company deriving more than 5

per cent of its revenue from defence.

But the war prompted SEB to change its tune. From April 1, six SEB

funds were allowed to invest in the defence sector. The bank says it

began to review its position in January as a result of “the serious

security situation and growing geopolitical tensions in recent

months,” which culminated in Russia’s invasion of Ukraine.

SEB is one of the few financial services companies to have announced a

change in stance, but the debate on the social utility of armaments is

now a live discussion among many large stewards of capital. The war in

Ukraine has accelerated a rearmament policy in Europe and defence

companies have outperformed global markets by the greatest margin in

almost a decade.

Some believe that defence companies ought to now be classified as

sustainable, allowing ESG investors to support the armament of

sovereign states against an aggressive neighbour.

Artis Pabriks, Latvia’s defence minister, recently took aim at Swedish

banks and investors, who refused to give a loan to a Latvian defence

company due to “ethical standards”. He said: “I got so angry. How can

we develop our country? Is national defence not ethical?”

A thornier issue is energy. Just as defence companies have soared, the

conflict has caused oil and gas companies to skyrocket, as prices

surge on concerns over Russian supply. This has tested responsible

investors — who typically are underweight oil and gas companies in

their portfolios — as they have underperformed conventional funds.

This dilemma presented by rising energy prices was evident in separate

statements in May by BlackRock and Vanguard, the world’s two largest

asset managers, who between them have almost $18tn in assets under

management.

Vanguard said it had refused to stop new investments in fossil fuel

projects and to end its support for coal, oil and gas production.

Meanwhile BlackRock announced that it was likely to vote against most

shareholder resolutions brought by climate lobbyists pursuing a ban on

new oil and gas production.

The warning appeared to mark a dramatic change in stance by the

world’s largest asset manager, whose chief executive Larry Fink has

been beating the drum for sustainability for years and presented the

group as playing a central role in financing the energy transition.

Activists worry that BlackRock’s move could grant permission for other

investors to loosen their grip on pushing companies to cut carbon

emissions. Critics say that it reflects how, amid surging oil prices

following Russia’s invasion of Ukraine, fossil fuel investments are

simply too lucrative for investors to ignore.

From an investor perspective, some are becoming increasingly sceptical

about the E in ESG. Stuart Kirk, global head of responsible investing

at HSBC’s asset management division, was suspended by the bank on May

22 after stating in a speech that climate change does not pose a

financial risk to investors.

But many investors remain optimistic about the longer term shift to

renewables. Carsten Stendevad, co-chief investment officer for

sustainability at hedge fund Bridgewater Associates, says that for the

energy transition, the war in Ukraine is “short-term painful”.

“The consumption of fossil fuels will increase. For Europe in

particular, green ambitions are now aligned with national security

ambitions and securing energy sovereignty, and that’s a pretty strong

trio,” he says. “This will accelerate the transition to renewables

because never again will countries want to be reliant on another

country for energy.”

The war has brought another question to a head: should responsible

investors exclude entire countries from their investable universe?

Although Russia only accounts for about 1.5 per cent of global gross

domestic product, data compiled by Bloomberg found that funds claiming

to promote or pursue ESG goals under an EU regulatory framework held

at least $8.3bn in Russian assets. Their holdings included Russian

state-backed companies such as Gazprom, Rosneft and Sberbank, as well

as Russian government bonds.

“For ESG investors, the conflict is something of a reminder that

actually sovereign risk is a really important input in ESG analysis,”

says Luke Sussams, ESG and sustainable finance analyst at Jefferies.

Since the war began, international corporations including Renault,

Shell and McDonald’s have marked a retreat from Russia. Many investors

disposed of the Russian sovereign debt holdings after the 2014

annexation of Crimea. And for most international investors, Russian

holdings represent a small slice of overall assets. The majority have

pledged not to make any new investments into Russian securities, but

divestment is more complicated because the market is in effect closed.

But if investors push to exclude entire countries on ESG grounds, what

does it mean for countries such as China — the world’s second-largest

economy — and Saudi Arabia, which have dubious environmental and human

rights records but considerably more strategic importance globally?

“I think there’s a really difficult judgment for an investor to make

here because on the one hand, some would say it’s unfair to attribute

all the ills of a government to its country’s business community,”

says Chuka Umunna, a former MP and shadow business secretary, now

leading ESG policy in Europe for JPMorgan. “But others say that by

continuing to do business with firms in that jurisdiction, you’re

helping to prop up the government . . . Where you draw the line in all

of this is not always straightforward.”

LGIM’s Laud says that investors should distinguish between a virtual

pariah state like Russia and China, where geopolitical tensions are

high but trade flows remain fluid. “Sanctions have been applied

internationally to Russia and it’s in an open conflict — this provides

a very different backdrop,” she says.

“There are reported issues in China but there have been in a lot of

countries. In order to establish the right investment approach a fair

and transparent sovereign scoring methodology needs to apply to every

country. Investors should differentiate between the sovereign, state-

owned enterprises and the broader corporate sector.”

Unstable environment

The war may have provoked a rethink in what ESG stands for, but the

challenge is compounded by the fact that there is no universal,

objective, rigorous framework for ESG investing.

In a recent paper, researchers at MIT and the University of Zurich

examined data from six prominent ESG rating agencies and found the

correlations between their assessments fall between 0.38 and 0.71 —

relatively weak, compared with the 0.92 correlation between credit

rating agencies. This, conclude the authors, “makes it difficult to

evaluate the ESG performance of companies, funds and portfolios”.

Regulators are trying to catch up. The UK and the EU are planning to

tighten the rules for ESG rating agencies, and the US Securities and

Exchange Commission recently levelled a $1.5mn fine at the fund

management arm of BNY Mellon for allegedly providing misleading

information on ESG investments.

The investigation into DWS will be closely watched as a test case

because it could herald a wider regulatory crackdown on ESG, which

some have warned might be the next mis-selling scandal, similar to

those in PPI, endowment mortgages or diesel cars.

Yet at the same time, the watchdog probing DWS — German financial

regulator BaFin — recently shelved plans to lay out rules for

classifying funds as sustainable.

“Against the backdrop of the dynamic situation in regulation, energy

and geopolitics, we have decided to put our planned directive for

sustainable investment funds on hold,” said BaFin president Mark

Branson. “The environment isn’t stable enough for permanent

regulation.”

Amid all this uncertainty, and with faith in ESG investing as a

catch-all term eroding, how should investors react? David Blood, who

founded sustainable investing pioneer Generation Investment Management

with former US vice-president Al Gore, says the biggest mistake

investors make is to try to boil down ESG to a checklist or an index.

“That checklist is a blunt instrument that doesn’t reflect the

challenges, subtleties and trade-offs of ESG,” he says. “People say

sustainability or ESG is always a win-win — of course it isn’t. There

are trade-offs.”

Crucially, the war in Ukraine and the debate around ESG categorisation

mustn’t allow investors to lose sight of the broader imperative to

decarbonise rapidly, Blood says. “The urgency and the business case

for the energy transition is absolutely intact and we mustn’t lose

sight of that ever.”

Asset managers say that, in the absence of clarity from authorities or

regulators, the key for them as responsible stewards of capital is to

be transparent about the criteria by which they are investing. It is

then up to clients to make a decision on whether to allocate money

based on their own ethical stance.

“We must not mix up ethical with ESG, because they are two separate

things,” says Saker Nusseibeh, chief executive of Federated Hermes.

“Being ethical is the prerogative of the client.”

Copyright The Financial Times

Limited 2022. All rights reserved.