New Tactics and ESG Themes Change the

Direction of Shareholder Activism

Posted by Richard J. Grossman and Neil P.

Stronski, Skadden, Arps, Slate, Meagher & Flom LLP, on Friday,

February 26, 2021

Takeaways

-

Activism is

likely to rebound as the business world recovers from COVID-19 disruptions.

-

Some activists

are raising permanent capital, giving them new leverage, and activist

approaches have become more acceptable to many institutional investors.

-

Even

high-performing companies may face pressure on ESG issues.

-

The best

defense is a solid relationship with and understanding of your shareholders,

coupled with a plan for dealing with activists if they emerge.

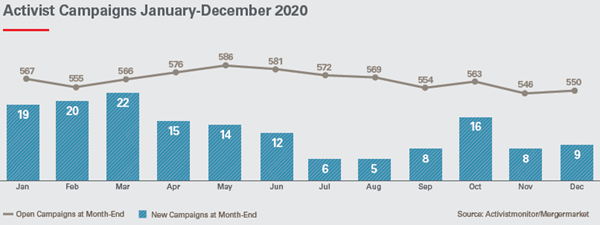

Shareholder

activism levels decreased in 2020 amid the upheaval and uncertainty brought on

by COVID-19. But activists did launch a number of high-profile campaigns and

there was an uptick of activism in the second half of the year; and more than 80

CEOs were replaced during activist campaigns.

Today, even

well-performing companies may find themselves targets of activist campaigns on

environmental and social issues, as new funds have been formed to specialize in

these areas. Moreover, established activists have established new types of

investment vehicles that could strengthen their hands. Preparing for the

possibility of an activist campaign should therefore be on the board agenda at

most public companies.

Expect an uptick

in activism in 2021. Historically,

many activist campaigns have focused on M&A and returns of capital. The economic

uncertainty and liquidity issues companies faced in 2020 reduced M&A activity

and made it harder for activists to advocate transformative deals, such as the

sale of a company, a breakup or major divestiture, or a large dividend payout.

In addition, there were fewer announced deals for activists to challenge.

As the economy

rebounds and business becomes more predictable, activists are likely to press

companies to undertake transactions and advocate for changes to the deals

companies propose.

COVID-19 problems

may spur some campaigns. Underperformance

is another traditional target of activists. As businesses struggle to cope with

the challenges of the pandemic, or if a company’s stock price does not return to

pre-pandemic levels, some could find themselves vulnerable to activists pressing

for operational or governance changes.

Even companies

with solid financial performance may face activists. Environmental,

social and governance (ESG) themes featured prominently in 2020 activist

campaigns, and several factors are likely to accelerate that trend.

Many

institutional investors, even managers of passive index funds, have called for

the business world to address environmental and social issues such as diversity.

(See “ESG:

Many Demands, Few Clear Rules.”) Major American and European oil

companies, for instance, have been pressed to lower their emissions by activist

groups that are backed by major pension funds and asset managers.

Some established

activists have recently formed ESG-focused funds alongside their regular pools

to target companies they contend have not met ESG standards, and some veteran

activists, including ValueAct founder Jeff Ubben, have formed new ESG-only

activist firms. Other new ESG funds have been formed by groups with few ties to

established activist firms.

Boards need to

prepare for this new set of players and their agendas, paying close attention to

their companies’ ESG profiles and ratings, and not just the financial

vulnerabilities that traditionally attracted activists’ attention.

The lines between

activists and other investors are blurring. A

number of major activist firms have begun acting more like private equity firms,

pursuing outright acquisitions or negotiating for large stakes in companies for

extended periods (private investments in public entities, or PIPEs). In 2020,

three of the best-known names in activism, Pershing Square, Starboard Value and

Third Point, formed SPACs (special purpose acquisition companies), shell

companies that raised capital to buy businesses. One of the most influential

established activist firms, Elliott Management, formed a buyout fund in 2019.

Meanwhile, some

private equity firms have pursued more activist-like strategies, and in some

cases, activists have teamed up with strategics or private equity firms on

acquisitions. Since activists often zero in on management and operational

shortcomings, a buyout is a logical next step.

These moves may

alter the calculus for companies in some situations, because an activist

investor with sufficient capital and a proven willingness to take a long-term

position in a company or to take it private poses a more serious threat than one

known only for saber-rattling and then trading out of the stock.

Traditional

investors have become more open to activism. Over

the last few years, as activism has become more accepted, some long-only asset

managers, including money managers, have supported activist campaigns where they

thought it would increase the value of their investments. Usually, this has been

behind the scenes, but some traditional asset managers have now openly adopted

activist tactics. For example, Wellington Management, the largest shareholder of

Bristol-Myers Squibb, came out against the drugmaker’s $74 billion deal to buy

biotech Celgene in 2019.

This reflects a

broader transition to a more shareholder-centric model of corporate governance.

Potentially, any investor with a clear agenda, sufficient resources and the

support of a wide shareholder base can utilize activist tactics.

Framing a Strategy

Given the

evolution of activism, it is vital for boards to ensure that their companies

have strategies to address activist pressure.

Shareholder

engagement is the best defense. Ongoing

dialogue with shareholders is the best preventive strategy. Know your most

significant shareholders and understand their investment theses. Engagement with

shareholders more broadly allows management to build relationships, articulate

the company’s strategy and establish the credibility that management and the

board will need in the event an activist surfaces.

Executives

usually take the lead in communications with shareholders, but direct engagement

by independent directors is becoming more common, particularly regarding

subjects under the board’s purview, such as executive compensation, capital

allocation and succession planning, and when a company is facing major

challenges. A company needs to weigh the pros and cons of using a director in

this role, and give careful thought to the choice of directors and prepare them

thoroughly.

Assess

vulnerabilities and prepare responses. Proactively

review your company’s vulnerabilities ahead of any activist approach, looking at

the business from the activist’s perspective. Consider whether alternative

financial and business strategies (say, a divestiture, spinoff or enhanced

return of capital) could boost shareholder value. An open-minded review can go a

long way toward reducing the risk of an activist intervention.

Develop a

defensive plan. Implement

a stock surveillance warning system to monitor new shareholdings, have a

shareholder rights plan ready to implement if an activist acquires a substantial

stake, assemble a team of advisers and prepare a playbook in case an activist

emerges. Another tool being used more frequently is a “table-top” simulation of

different activist scenarios to test and refine a company’s reactions.

Early board

involvement is critical. If

an activist surfaces, it is crucial that management alerts the board immediately

so directors are educated and are actively involved in the response. To avoid

missteps, the board and management must be aligned in their approach and

coordinate both internal and external communications.

* * *

|

Harvard Law School Forum

on Corporate Governance

All copyright and trademarks in content on this site are owned by

their respective owners. Other content © 2021 The President and

Fellows of Harvard College. |