THE

WALL STREET JOURNAL.

Markets

Stock Buybacks Are Booming, but Share Prices Aren’t Budging

Some

analysts worry companies are buying their shares at excessive

valuations, while others say cash could have gone toward capital

improvements

|

Bank of America is one of

several major companies buying back stock this year. PHOTO:

RICHARD B. LEVINE/ZUMA PRESS |

By

Michael Wursthorn

July 8, 2018 9:00 a.m. ET

U.S. companies are buying

back record amounts of stock this year, but their shares

aren’t getting the boost they bargained for.

S&P 500 companies are on track to

repurchase as much as $800 billion in stock this year, a record that would

eclipse 2007’s buyback bonanza. Among the biggest buyers are companies like Oracle Corp. , Bank

of America Corp. and

JPMorgan Chase & Co.

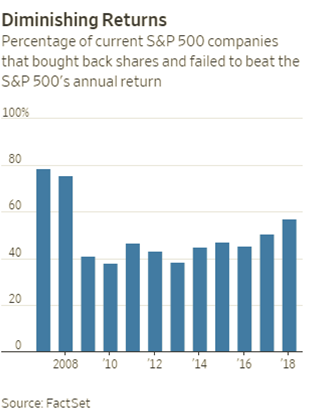

But 57% of the more than 350

companies in the S&P 500 that bought back shares so far this year are trailing

the index’s 3.2% increase. That is the highest percentage of companies to fall

short of the benchmark’s gain since the onset of the financial crisis in 2008,

according to a Wall Street Journal analysis of share buyback and performance

data from FactSet.

And the historic spending spree on

share buybacks has some analysts worried companies are buying their shares at

excessive valuations during the peak of the economic cycle and at a time when

the market rally is nine years old. Others warn the billions of dollars spent to

buy back shares could have gone toward capital improvements like new factories

or technology that could lead to stronger long-term growth.

“There has been less of a reward for

companies engaging in new buybacks over the last 18 months,” said Kate Moore,

chief equity strategist and a managing director at asset-management firm BlackRock Inc. “It’s

fair for investors to ask whether companies are buying at the right point.”

The S&P 500 Buyback index, which

tracks the share performance of the 100 biggest stock repurchasers, has gained

just 1.3% this year, well underperforming the S&P 500.

Share buybacks have become corporate

America’s go-to strategy for boosting stock prices and earnings over the past 30

years. The point of buybacks is to try to make a company’s stock more valuable.

By mopping up shares, a company shrinks the stock pie, which boosts earnings per

share. That, in turn, should push the share price higher.

The potential problem: Executives

directing buybacks are essentially timing the market, and often they end up

buying high.

Buyback activity reached a frenzy in

the early 2000s; the previous record for share repurchases was $589.1 billion in

2007. But that was just a year before the stock market tumbled into the worst

financial crisis since the Great Depression. The result: companies like Exxon

Mobil Corp., Microsoft Corp.

and International

Business Machine Corp.

each paid more than $18 billion to repurchase stock at a peak, only to see their

share prices slump a year later.

Stock buybacks appear just as

ill-timed now, some analysts and investors say, especially as companies ramp up

spending after last year’s $1.5 trillion tax overhaul put extra cash in their

coffers.

Oracle has been one of the biggest

buyers of its own stock in recent years and spent

$11.8 billion on stock repurchases last year, when shares gained

nearly 23%. But that gamble hasn’t looked smart this year as the

networking-device maker has struggled alongside the broader market, pulling its

shares down 6%.

Still, Oracle’s board approved a

fresh round of share buybacks totaling $12 billion in February, and executives

appear to have spent nearly half that sum already. A representative from Oracle

declined to comment on its share buyback program, but the company said in a

recent Securities and Exchange Commission filing that it “cannot guarantee” its

share repurchase “will enhance long-term stockholder value.”

Others like McDonald’s Corp. ,

Bank of America and JPMorgan Chase have spent

billions on share repurchases this year, but haven’t seen a

short-term bounce in share prices. McDonald’s bought back $1.6 billion of shares

in the first quarter, but the fast-food chain’s stock is down 7.4% this year.

Bank of America and JPMorgan

Chase have both spent more than $4.5 billion to buy back their

shares, which are down 5% and 2.7%, respectively.

All three companies also spent

multibillion-dollar sums on buybacks in 2017 as the stock market hit repeated

highs.

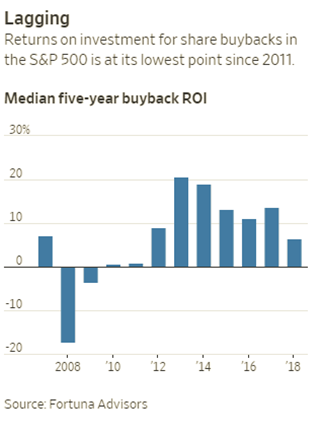

Companies in the S&P 500 that have

repurchased shares are expected to see a return on investment of about 6.4% this

year, a percentage that falls below the past six rolling five-year periods as

measured by Fortuna Advisors, a financial consulting firm that has examined

buyback trends going back to 2007.

Returns on investment for buybacks

peaked in 2013, according to Fortuna’s analysis, as companies used share

repurchases to boost earnings and dig themselves out of the depths of the

financial crisis. With stock prices relatively low at the time and economic

activity tepid, share buybacks were one of companies’ key sources of earnings

growth.

But even as the stock market

steadied in the subsequent years and economic growth around the world picked up

to help boost profits, corporate executives continued to spend wildly on share

repurchases—often at the expense of other types of spending, including dividends

and capital improvements. Spending on capital expenditures rose to $166 billion

in the first quarter, up 24% from a year earlier, according to Credit

Suisse , but

still well below the $189 billion spent on buybacks.

“The majority of capital deployed is

going right back to shareholders and not reinvestment in businesses,” said

Gregory Milano, chief executive at Fortuna. “If that’s the only thing you’re

relying on, it’s going to end badly.”

Some share buybacks do pay off, but

that tends to be among companies that show a high level of sales and earnings

growth on their own, analysts say. Apple Inc.,

for example, has bought

back $22.8 billion worth of stock so far this year. Its shares have

risen 11%, with much of the boost coming after it reported strong gains in

second-fiscal-quarter revenue and profit—as well as a record $100 billion plan

to buy back more stock.

“Corporate America has such an

obsession with bottom-line growth,” said Jay Bowen, president of Bowen Hanes &

Co., manager of the $2 billion Tampa Firefighters and Police Officers Pension

Fund. “Long term, I don’t like it.”

Write to Michael

Wursthorn at Michael.Wursthorn@wsj.com

Appeared in the July 9, 2018, print edition as

'Stock Prices Defy Surge in Buybacks.'