|

THE

WALL STREET JOURNAL.

Markets

Don’t Make Me Do This: Rise of the Reluctant Activist

Some typically passive investors are adopting the tactics of

activists

|

Daniel O’Keefe’s investment firm Artisan Partners earlier this

month publicly urged Johnson & Johnson to separate its three

main businesses. Above, Mr. O'Keefe attended a conference in Sun

Valley, Idaho, in 2013. PHOTO: BLOOMBERG |

By

David Benoit

Updated Feb. 18, 2016 7:41

p.m. ET

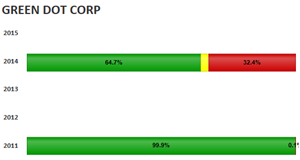

Investor Jeffrey Osher

sat on his holdings in prepaid-debit-card issuer

Green Dot Corp.

for three years before he lost his patience.

In December, after a

string of disappointing earnings reports that left the company’s

shares down sharply, the hedge-fund manager met with the board and

asked directors to fire founder and Chief Executive Steven Streit,

according to people familiar with the meeting. When the board refused,

Mr. Osher’s Harvest Capital Strategies LLC did something it had never

done before: It publicly threatened to run a campaign to oust the

company’s directors.

Those moves put Mr.

Osher into a newly emerging class of shareholders: Typically passive

investors who are adopting, sometimes reluctantly,

the tactics of activists.

The rise of these

“reluctavists” or “suggestivists,” as they are sometimes called,

reflects the success of vocal shareholders in forcing corporate

change, as well as broader shifts in the investing world. Changes in

securities laws and an expansion of investor rights have encouraged

shareholders who once deferred to management to speak up when they are

unhappy.

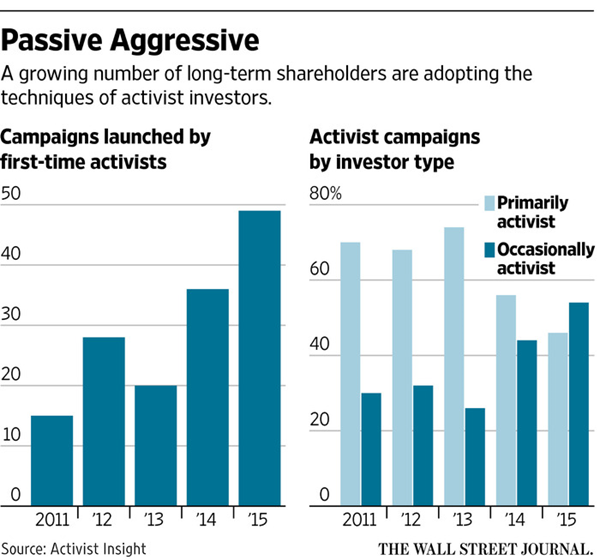

First-time activists ran

49 campaigns against U.S. companies last year, up from 36 in 2014 and

15 in 2011, according to Activist Insight. Some 54% of all campaigns

were launched by what the researcher deems “occasional” activists, up

from 30% in 2011.

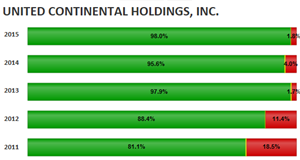

Two longtime airline

shareholders recently changed their status to active investors from

passive at

United Continental Holdings

Inc.,

the parent of United Airlines, indicating they plan to raise their

voices on strategy and management. Canyon Capital Advisors LLC has

joined

a chorus of activists pushing

Yahoo Inc.

to

change direction, a rare move for the $24 billion fund.

| |

Harry Wilson last year led several large investors in a

successful push to get General Motors Co. to buy back more

shares.

Photo: Michael Nagle/Bloomberg News

|

Harry Wilson, an

architect of the Obama administration’s restructuring of

General Motors Co., last year

led several large investors in a successful

push to get GM to buy back more shares.

Angie’s List Inc.,

meanwhile, is facing a possible fight for board seats after resisting

a sale backed by TCS Capital Management LLC, an investor that first

took a stake in the consumer-review website before its 2011 initial

public offering.

“These are long-term

investors who have reached a point where they see opportunities for

value that the company isn’t pursuing and after years of

underperformance they are putting themselves out there,” said Andrew

Freedman of law firm Olshan Frome Wolosky LLP, which represents

activist investors, including some first-timers. “They aren’t just

short-term value seekers. They are the long-suffering shareholder.”

Whether this new crop of

investors will find the same success as dedicated activists remains to

be seen. While there are notable exceptions, such as

John Paulson’s Paulson & Co.,

most occasional activists lack the name recognition and track record

of established activists like

Carl Icahn or

William Ackman.

Furthermore, these

investors often have smaller stakes in the companies they target.

Daniel O’Keefe’s $32

billion investment firm Artisan Partners earlier this month publicly

urged

Johnson & Johnson

to

separate its three main businesses. Artisan has a 0.2% stake in the

health-care company, which has a market value of $284 billion.

‘Like most people, I don’t

welcome battles.’

—George Young, chief compliance officer at Villere

|

|

J&J has met with Mr.

O’Keefe several times, but it is standing by its corporate structure.

“These are not decisions

that I came to on a whim,” Mr. O’Keefe said. “These are conclusions

that I came to after years of following the company and considering

counterpoints.”

Funds wading into

activism for the first time say the experience can be eye-opening.

Take St. Denis J.

Villere & Co., a 105-year-old New Orleans investment firm whose first

foray into activism landed it in court. The family-run firm in 2014

raised concerns about legal-software company

Epiq Systems Inc.

after 11 years of investing in the stock. The two sides later reached

an agreement to put a Villere ally on the board as Epiq launched a

strategic review.

But a year later, that

process had stalled, and Epiq’s results disappointed the investor.

Villere nominated six directors to the company’s nine-member board in

December.

Epiq, while saying it’s

open to shareholder input, said the nominations violated the earlier

settlement. Epiq and Villere have traded lawsuits. The company

recently named a new lead independent director and replaced two board

members.

George Young, Villere’s

chief compliance officer and a member of its founding family, said a

long-running evolution of U.S. securities law has spurred Villere to

think more about how it votes its shares. That, in turn, has led it to

get more aggressive with management teams.

But future public

campaigns are a different story. Mr. Young, who often carpools to work

with his uncles and cousins, said he was unaccustomed to the

round-the-clock demands of an activist fight.

“Like most people, I

don’t welcome battles,” he said.

Mr. Osher said he, too,

would rather operate behind the scenes. But he felt Harvest, one of

Green Dot’s largest shareholders, needed to publicly state its case.

On Jan. 25, the 16-year-old San Francisco investment firm released a

93-page presentation criticizing Green Dot’s performance. It also

directed shareholders to a website, www.fixgdot.com, that urged the

company to immediately remove Mr. Streit.

Green Dot said its board

and management held “numerous” calls and meetings with Harvest and

would “carefully review” the investor’s suggestions.

“I prefer to operate out

of the public eye,” Mr. Osher said. “I’m very disappointed this is the

avenue we had to pursue.”

Write to

David Benoit at

david.benoit@wsj.com

|