|

Barron's Cover

How

Nelson Peltz Gets Results

Nelson Peltz was an activist before

the term was popular. Targets like Pentair are bigger, but his aim is

the same: Cut costs, boost sales.

By

Jonathan

R. Laing

July 4, 2015

You’d think that Nelson

Peltz and his fellow operatives at Trian Partners would be down in the

dumps after recently losing a hotly contested proxy fight to win seats

on the DuPont board. That wasn’t the case when Barron’s met with Peltz

and his Trian hedge fund co-founders, son-in-law Edward Garden and

longtime business sidekick Peter May. They were upbeat, even defiant

in our discussions in their conference room on the top floor of a Park

Avenue office building.

|

Trian Partners’ Peltz: “Years of steady cash flow tend to dull

companies’ entrepreneurial fire…” Photo: Rick Wenner for

Barron's |

They had ample cause to be

bitter. Peltz, 73, would be on the DuPont (ticker: DD) board had just

one of the big index funds families, Vanguard Group, State Street

Global Advisors, or BlackRock, swung to Trian’s side, as most active

money managers did. Another 5% of the shares voting Peltz’s way would

have carried the day in what many viewed as an important test for

activist shareholders.

But the investor and his

colleagues obviously were ready to move on. Last week, they revealed a

new stake in pump and valve maker Pentair (PNR), and they haven’t

forsaken DuPont. “At least we’ve succeeded in educating DuPont’s board

and shareholders so they won’t continue to accept mediocre earnings

performance by the company. We won’t be the only ones monitoring the

company and its management,” says Peltz.

Their $1.5 billion DuPont

stake will probably remain, they say. In their estimation, the

position is likely to keep the pressure on DuPont Chairman and CEO

Ellen Kullman to follow the Trian plan of cost-cutting and business

restructuring. Should Kullman fail to perform, there’s always a

chance, says one Trian exec, that the firm may mount another proxy

fight. Notably, DuPont’s stock fell 7% on the day Trian lost, and it

has yet to recover.

Aside from Pentair, the

Trian trio indicated they’re taking positions in two other large

companies in need of a shake-up, though they won’t say what they are.

They have a war chest of over $3 billion in cash to deploy from their

$12 billion in assets under management.

PELTZ HAS COME A LONG

WAY since the mid-1980s, when he was considered a lesser light in

the Drexel Burnham Lambert galaxy of junk-bond-financed raider stars

like Carl Icahn, Ronald Perelman, Saul Steinberg, and T. Boone

Pickens.

Peltz never quite fit the

buccaneer mold of many of Drexel junk-bond chief Mike Milken’s

raiders. Peltz didn’t do greenmail deals like the others, buying a

position in a target company and then threatening a takeover if it

didn’t buy back the shares at higher-than-market price. “We actually

wanted to own companies and had confidence that we could operate them,

and this made some of the Drexel fold a bit worried,” he recalls.

Decades later, he’s still

trying to spruce up companies through judicious cost-cutting and

aggressive marketing and capital spending, though given the size of

his targets, he has to operate from a minority stock position. While

private-equity folks and other leveraged artists take all of the

profits in their deals, Peltz, May, and Garden allow fellow

shareholders to participate, too.

Since founding the Trian

Partners hedge fund family in 2005, Peltz and May, now 72, have

wielded a much bigger stick on Wall Street than they did in the 1980s

and 1990s. Trian was instrumental, for example, in pushing the food

company Kraft in 2012 to split for efficiency’s sake into a domestic

unit, Kraft Foods (KRFT), and a faster-growing foreign unit dubbed

Mondelez International (MDLZ). Peltz, May, Garden, and others close to

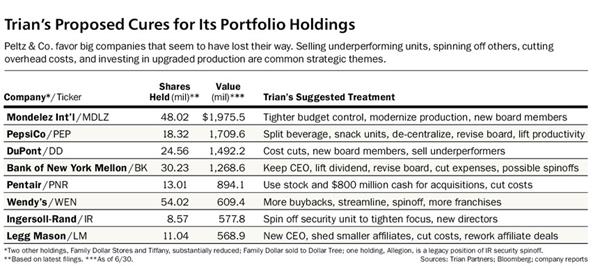

Trian have served on the boards of well-known companies like PepsiCo

(PEP), Mondelez, Bank of New York Mellon (BK), asset-manager Legg

Mason (LM), retailer Family Dollar Stores (FDO), toolmaker

Ingersoll-Rand (IR), and Tiffany (TIF) to further Trian’s activist

agenda.

Prior to the DuPont

dust-up, Trian had faced only one proxy fight to achieve board

representation. That was in 2006, when Heinz fought against Trian’s

proposed slate of five new directors. Peltz and another slate member

won.

Peltz was able to win over

Heinz CEO Bill Johnson and the Heinz board with his prescription of

cutting extraneous expenses and pushing the savings into more

aggressive marketing and plant and product expansion. “Of course, we

all had a certain view of Nelson and his supposed raider past, but he

turned out to be a wonderful addition to the board,” Tom Usher, former

chairman of U.S. Steel and then lead director at Heinz, recalls to

Barron’s. “He was always well informed and collaborative and not given

to throwing his weight around or grandstanding.”

Echoes Johnson: “I

developed the utmost respect for him.” Peltz, in fact stayed on the

Heinz board even after Trian exited the bulk of its Heinz position,

and he helped the board vet the rich leveraged buyout of the company

by the Brazilian private-equity firm 3G and Warren Buffett–led

Berkshire Hathaway (BRK.A). Johnson has since become a Trian Advisory

Partner (a small group of former CEOs who work with the firm) and was

recently added to the PepsiCo board.

What Trian calls its

“constructivist activist” approach seems to have served both his hedge

fund partners and target companies well. Since its 2005 inception to

May 30, 2015, a decade in which indexes topped stockpickers, Trian

notched decent annual net returns of 9.7%, compared with an 8.26%

return for the Standard & Poor’s 500 and a 4.8% annual return for the

HFRI Equity Hedge Fund Index. (Trian was No. 87 this year on

Barron’s Penta’s Top 100 Hedge Funds with an annualized

three-year compound return of 15.99%.) Trian’s only losing year came

during 2009’s vicious market selloff, when it lost 17.21%. The S&P and

HFRI returns plummeted 37% and 26.65%, respectively, that year.

|

After DuPont

defeat, Trian founders, from left, Peltz, Edward Garden, and

Peter May moved on quickly. Photo: Rick Wenner for Barron's

|

DECADES BEFORE THEY

COULD contemplate targeting DuPont, Peltz and May were running a

frozen-food distribution company called Flagstaff. May, a former Peat

Marwick accountant, had come on board in 1972 to help take public the

Peltz family’s enterprise, which Nelson had been building since the

1960s.

It wasn’t an easy ride.

And by the early 1980s, the fledgling Peltz-May empire nearly crashed,

after the pair sold Flagstaff to a takeover group that came up short

on a promised payment. The business ended up in Chapter 11 in 1981,

laid low by soaring interest rates and operating miscues.

A lifeline of a sort came

in 1983 when Peltz and May were able to use bank debt granted under

onerous terms to buy a controlling interest in a New Jersey wire and

cable and vending-machine outfit called Triangle Industries. Triangle

was losing money but had a decent balance sheet. “I remember telling

my wife that we were putting all our chips on the table in the deal,

and if it didn’t work, I could always go back to being a public

accountant,” recalls May.

Peltz wasn’t that

optimistic. After giving a Manhattan panhandler a buck, he mused to

his new wife, fashion model Claudia Heffner, that the vagrant now had

a bigger net worth than they did.

They were able to turn

Triangle’s operations around in less than a year, says Peltz. Their

first coup came in the mid-1980s when Peltz and May linked up with

Milken and Drexel to buy National Can Company for $460 million and

then, a year later, American Can for $570 million for Triangle. “If

the truth be told, our leverage on the National deal was infinite

since our equity layer was all borrowed, too,” May remembers with a

slight chuckle.

But the packaging

companies prospered as a result of cost-cutting combined with an

audacious, junk-bond-fueled capital-spending program for new plants.

In 1988, the French firm Pechiney bought the American National

operation for $3.9 billion, including assumed debt, resulting in a

combined personal payday for Peltz and May of about $900 million.

Peltz reminisces on those

days: “We weren’t greenmailers like so many of the Drexel corporate

raider crowd.” Even so, he adds, “I owe a lot to Mike Milken and have

remained close to him and his charitable work and foundation.”

The next big score came in

1997, when an entity that Peltz and May controlled, Triarc, bought

Snapple from Quaker Oats for $300 million, $1.4 billion less than

Quaker had paid for the company in 1994. In less than three years, by

cutting corporate overhead and reviving the edgy Snapple marketing

culture, sales volume revived and earnings surged. In 2000, Triarc

sold Snapple and a few smaller beverage brands to Cadbury Schweppes

for $1.45 billion, netting Peltz and May nearly $450 million.

THE DECISION IN 2005

to become a hedge fund was pushed by Peltz’s son-in-law, Garden, now

54, who had joined Peltz and May two years before. “I had a ‘come to

Jesus moment’ that we had to attract outside capital, as private

equity and hedge funds were doing, to operate on the scale necessary

to invest in more and bigger targets,” says Garden, a former

investment banker.

With its $12 billion of

mostly institutional money, Trian has become a powerful force in

activism’s most potent era. Its clientele include many major pensions,

endowments, and even some sovereign wealth funds. Much of the money

has lockup provisions of five years or more, giving Trian plenty of

time to work its strategies on different companies.

Trian’s activist style is

attractive to both investment partners and target companies.

Institutions like investing in mostly staid blue-chip companies that

come with an informal management-consulting group -- Trian -- trying

to squeeze out better results. Trian also provides management with the

cover to make bold corporate cuts and other tough decisions.

The firm likes companies

that, after decades of success, have begun to rest on their laurels.

Peltz elaborates, “Years of steady cash flow tend to dull companies’

entrepreneurial fire and focus on having best-in-class profit margins

and revenue growth. Top-heavy corporate structures result,

characterized by layer upon layer of bureaucracy anxious to justify

their very existence. Accountability erodes as key decisions, such as

where to spend research-and-development, capital expansion, marketing,

and advertising dollars, devolve more and more from operating units to

headquarters. Special constituencies and interest groups develop to

subvert any attempt at zero-based, or what we at Trian call

white-sheet, budgeting, in which every expense has to be justified as

enhancing profitability and growth.”

TRIAN AND OTHER

ACTIVISTS have critics. Bill George, a Harvard Business School

senior fellow and the former chairman and CEO of medical-device maker

Medtronic, claimed in a blog post that DuPont’s proxy victory should

embolden other companies to stand up to the bullying tactics of

aggressive activists like Trian. DuPont was controversial, in part,

because the stock has risen in the past three years. Others, such as

fund powerhouse BlackRock’s chief Laurence Fink, claim that too many

activists do “smash and grab” attacks on corporate balance sheets,

either forcing companies to siphon off excess cash or incur more debt

to buy back stock or boost dividends to push the stock price

temporarily higher. All of this can adversely affect the long-term

competitive future of Corporate America by causing companies to give

short shrift to capital spending and R&D, these critics contend.

Trian officials say that

much of the cost-cutting they push is designed to be redeployed into

growth initiatives like plant expansion and more-aggressive marketing

budgets. Likewise, they typically hold stock positions for years,

since makeovers of income statements to boost operating margins can’t

be achieved quickly.

Finally, their stakes in

large companies like Pepsi and DuPont -- just 1% and 3%, respectively

-- are small relative to their huge valuations. “Even when we serve on

boards, we can only win over management and other directors with the

power of analysis and argument,” Peltz observes. And, perhaps most

interesting, if Trian succeeds in its activist makeovers, fellow

public shareholders get to participate in the upside.

Regardless of a losing

proxy vote, Trian has influenced all of the companies in which it

holds stakes, the biggest of which, ranging from $1.5 billion to $2

billion, are DuPont, PepsiCo, and Mondelez. Trian takes credit for

pressuring a reluctant DuPont board and management into a number of

shareholder-friendly moves since Trian’s investment was reported in

early 2013.

Among other things, DuPont

has announced about $1 billion in long-overdue cost cuts, and just

last week spun off the Chemours unit that produces products like

Teflon. It also upgraded its board of directors to include two

respected executives from outside the company, Tyco’s Edward Breen and

former LyondellBasell chief James Gallogly, whom Trian has consulted

with previously. DuPont has also disclosed plans to return $9 billion

in capital to shareholders.

DuPont, of course, doesn’t

see Trian’s hand in these decisions. The company says they were part

of a restructuring plan that CEO Kullman launched when she was named

to the top job in January 2009. Yet, Trian officials insist that much

more remains to be done to boost profit margins and revenue growth to

peer levels, including making $2 billion to $4 billion in cost cuts

and hiving off poorly performing business lines.

PepsiCo has been a tough

nut for Trian to crack since the fund first disclosed its stake in

early 2013. The Pepsi board and the company’s charismatic Chairman and

CEO Indra Nooyi turned down Trian’s suggestion to separate its

fast-growing snack-food operation, Frito-Lay, from the beverage

business to unlock shareholder value.

But a truce was reached

this year when Pepsi agreed to put Trian Advisory Partner Johnson on

its board. Trian is also heartened by Pepsi’s moves to return more

money to shareholders and begin a five-year, $5 billion

productivity-enhancement program. “PepsiCo needs to return to its

roots as a company that was lean at the corporate level and gave

virtual autonomy to hard-charging, able executives at the beverage,

snack food, and, until 1997, fast-food operation [since spun off],”

says a Trian exec.

Trian acquired a stake in

Mondelez after the global seller of everything from Cadbury candies to

Oreos to gum separated from Kraft in 2012. Ever since, Mondelez

management has embraced much of the Trian playbook by adopting

zero-based budgeting and investing in new high-tech plants to bring

down production costs. The moves are starting to improve operating

profit margins and earnings on a constant currency basis. Peltz joined

the Mondelez board in early 2014.

Expect a similarly

friendly approach with Pentair, whose valves and pumps are used on

farms, at food and beverage makers, and in wastewater-treatment

plants, among other deployments. Trian would like the company to tap

$800 million in cash and a tax-advantaged base in the United Kingdom,

to make more acquisitions and grow.

THESE DAYS, TRIAN’S

OFFICES exude an air of establishment respectability, with lots of

sedate wood paneling, muted fabric wallpaper, and architectural

renderings of 19th century Beaux Arts buildings culled from May’s

private collection. The firm makes a big deal of the rigor of Trian’s

research. In all, 14 Trian partners and squads of analysts churn out

white papers, examining in minute detail how target companies stack up

against rivals, employing dozens of metrics and offering rafts of

remedies to improve performance.

That’s not to say that

Peltz doesn’t cut a larger-than-life figure. He displays all the

trappings of a billionaire. There’s his private jet and the fancy SUV

that takes him to New York City daily from his 130-acre estate in

Westchester County’s Bedford, N.Y., which features a lake, a

waterfall, and a large indoor skating rink he built for his kids. He

also owns an opulent French Regency–style home in Palm Beach, Fla.,

that sits on 15 acres fronting the Atlantic Ocean.

Yet, Peltz is a devoted

family man who ferries his children to hockey games and other sporting

events. He has 10 children ranging in age from 50 to 12. Eight of them

are from his third marriage, to Claudia, to whom he has been wed for

over 30 years. “That number is a bit deceptive,” he explains in his

gravelly voice. “They include two sets of twins. I’ve always liked

leveraging productivity. One delivery room, one doctor, and two kids.”

He’s quick to acknowledge

that he was not as good a student as his children were. Peltz was a

college dropout (“I was a ski bum at the time”), but a number of his

kids made it to the Ivy League, including three graduates of Yale

University. His daughter Nicola is a Hollywood actress with a recent

starring role in the fourth edition of Michael Bay’s Transformers

movie franchise, along with Mark Wahlberg.

Giving up on school, Peltz

joined his father’s company and found he had flair for both deal

making and operating businesses. His father’s guiding business

principle -- which he soon internalized -- was “sales up, expenses

down.”

That has remained his

mantra, albeit on successively larger stages. He and his hedge fund

will keep trying to make it work for its large corporate targets.

|