|

THE

WALL STREET JOURNAL.

Markets

Activist Funds Put Executive Pay Formulas Under Microscope

Marathon says it found a compensation scheme ‘run amok’ at

Shutterfly

|

An activist hedge fund said Shutterfly’s executive-pay plan

rewarded scale over profits. Above, Shutterfly boxes are

prepared for shipment in Phoenix. PHOTO: WILL SEBERGER FOR

THE WALL STREET JOURNAL |

By

Liz Hoffman

June 11, 2015 5:39 p.m. ET

Big shareholders for years have grumbled about the rise

in executive pay. Now, activist investors are taking up the

compensation cause, focusing less on how much corporate leaders earn

and more on whether they deserve what they get.

Case in point:

Shutterfly Inc.[ ],

where an activist hedge fund is

seeking three board seats at the

online photo retailer at a shareholder vote set for Friday. The

founder of Marathon Partners Equity Management LLC said once the fund

“started peeling back the onion” on Shutterfly’s pay plans, it found

“a compensation scheme that had run amok.” ],

where an activist hedge fund is

seeking three board seats at the

online photo retailer at a shareholder vote set for Friday. The

founder of Marathon Partners Equity Management LLC said once the fund

“started peeling back the onion” on Shutterfly’s pay plans, it found

“a compensation scheme that had run amok.”

Marathon’s main complaint, that the company rewards

scale over profits, is finding increasing resonance among activists

lately. Shutterfly has defended its pay plan, while it recently

tweaked the metrics it uses to determine pay. Changes to the plan

“appropriately reflect stockholder views while also balancing the

critical importance of retaining key employees,” the company has said.

Once left to governance hounds, unions and academics,

executive pay is getting a closer look from activist investors, which

take stakes in companies and push for measures to boost share prices.

These funds are scanning corporate filings for what they see as skewed

incentives and generous formulas, increasingly moving what had long

been a back burner issue to the fore.

“Compensation was not something activists cared about a

great deal, unless they could use it as a wedge to get something else

done,” said Francis Byrd, a former TIAA-CREF corporate-governance

expert. “That’s starting to change.”

Activists

have zeroed in on pay recently at

Qualcomm Inc.[],

DuPont Co.[]

and

Perry Ellis International Inc.[]

Some

activists argue that ill-designed plans encourage the wrong kinds of

growth—for example, boosting revenue at the expense of profitability.

Others point to nonstandard financial metrics they say reward

executives even when business falters. Criticisms tend to focus less

on the size of CEOs’ paychecks than on the yardsticks that determine

them.

Companies say such critiques are off-base and that

handcuffing pay packages makes it hard to retain talent. They also

note executive pay is mostly stock, which ties executives’ fortunes to

those of all shareholders.

Most activists are unlikely to pick fights based solely

on pay. Arguments about corporate operations are considered more

powerful, investors and advisers say. But more are embracing the idea

that incentives matter.

One factor teeing up the issue for activists is the

complexity of compensation, experts say.

“I’ve seen bonus plans that would take a Ph.D. in

physics to figure out,” said Kevin McManus, vice president at

shareholder-advisory firm Egan-Jones Ratings Co.

That complexity presents opportunity for activists, who

typically research a handful of companies, rather than monitor

hundreds. “You’ve got someone who has the time and the incentive to

dig into the numbers” Mr. McManus said.

Take Trian Fund Management LP, which

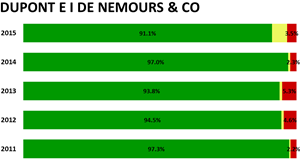

narrowly lost a DuPont []

shareholder vote for board seats in May. It has made a small

cause out of executive compensation, regularly seeking a seat on the

compensation committee of boards it goes on, according to people

familiar with its practices.

At DuPont, however, Trian criticized how the company’s

board calculated bonuses, drawing on scores for individual performance

and overall corporate performance. DuPont’s board in 2014 assigned

zero points for the latter, after earnings inched up just 3%, but gave

executives higher personal scores.

“How can it be that the company is doing poorly

operationally but management as individuals are each doing great?”

Trian said in shareholder materials.

DuPont recently changed its plan to give a heavier

weighting to the company’s overall performance and de-emphasize

individual scores. A spokeswoman said the plans “are designed to align

pay with performance and the achievement of annual goals and

objectives.”

Jana Partners LLC, which

recently took a $2 billion stake in Qualcomm[],

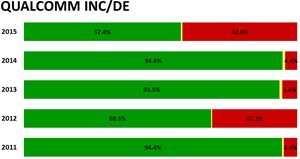

has urged the company to tie executive pay to measures like return on

invested capital, rather than its current yardsticks of revenue and

operating income, according to a Jana investor letter. Such changes

“would eliminate the incentive to grow at any cost,” said the letter,

reviewed by The Wall Street Journal.

Qualcomm has said its pay plans were aligned with

stockholders’ interests and cited the “increasing competitive threat

Qualcomm faces for talent.” An example: Its current chief executive

was courted by

Microsoft Corp., according to a

person familiar with the matter.

Another red flag for activists: metrics that change on

the fly.

In 2010, Perry Ellis linked bonuses for its

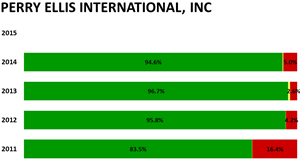

father-and-son management team to earnings before interest, taxes,

depreciation and amortization, a common measure of cash flow known as

Ebitda. By 2013, the retailer had fallen short of its three-year goal.

Meanwhile, a new phrase had appeared in the company’s

filings: “adjusted Ebitda.” Adding back in certain costs, the tweaks

pushed the company just above the threshold necessary for the two men

to receive their maximum bonuses of $1.4 million each.

Activist hedge fund Legion Partners LLC said in May the

change “undermines confidence” and wasn’t adequately disclosed to

shareholders. Legion, along with a California pension fund, had been

seeking board seats but dropped the fight last month after Perry Ellis

added new directors and announced a CEO succession plan.

A spokeswoman for Perry Ellis declined to comment on

the change. She said the executives didn’t receive a bonus in 2014 or

2015 after the company fell short of the new targets.

Perry Ellis recently revamped its bonus metrics again.

Executive bonuses will soon be based on total shareholder return and a

mix of earnings before taxes and return on invested capital—both “as

adjusted.”

The larger argument from activists—that pay too often

rewards size over profitability—echoes a common push among activists

to get

companies to slim down and focus.

In its early years as a fledgling technology company

Shutterfly needed scale, Marathon’s managing partner Mario Cibelli

said, so tying bonuses to revenue growth, among other measures, made

sense. Now, Shutterfly is a $1.7 billion company in a maturing

industry and should reward profitability, he argues.

Starting next year, Shutterfly will tie bonuses to

measures that more closely track profits, including free cash flow and

total shareholder return.

—Michael Rapoport contributed to this article.

Write to

Liz Hoffman at

liz.hoffman@wsj.com

|