|

Shareholder activism's impact on brand value

October 21, 2014

|

By David Bogoslaw

First study of activism and brand value finds predominantly negative

impact on brand value extending long beyond original activist campaign

There has been a lot of research in recent years showing that a

specific form of shareholder activism known as hedge fund activism has

had an adverse impact on shareholder value, as measured by stock price

performance and market cap, in the wake of an activist campaign.

Harvard Law School professor Lucian Bebchuk and his associates have

questioned the ‘scientific’ validity of this research from varied

sources, but he and his supporters are a small minority.

What hasn’t been studied until now, however, is the impact of

shareholder activism on corporate brand value. To produce this

research analysis, Corporate Secretary partnered with CoreBrand, a

natural choice given the latter’s impressive database of nearly 1,000

companies from 54 key industries and more than 20 years’ expertise in

studying the elements of brand value and advising clients on how to

strengthen their corporate brand and capitalize on their brand value.

Each year, CoreBrand surveys 10,000 business decision makers from the

top 20 percent of US businesses with annual sales above $50 million to

arrive at scores for familiarity and favorability, which reflect

company size/recognition and quality, respectively. Familiarity

represents a weighted percentage of survey respondents who recognize

the brand being evaluated. Only respondents who are familiar with a

brand – knowing more than just the company name – are asked to rate

the three dimensions of favorability on a four-point scale: overall

reputation, perception of management and investment potential.

Familiarity and favorability scores are then combined into a single

BrandPower score and the scores are used to calculate the brand equity

value (BEV) – comprising BrandPower, familiarity and favorability – of

each company, both as an absolute dollar value and as a percentage of

the company’s market cap.

Event-driven impacts

With data extending back to the early 1990s, CoreBrand is able to

measure changes in a company’s BEV from a specific event such as a

major earnings restatement or a CEO’s removal. This lets CoreBrand

determine the magnitude of the impact the event has had on BEV, both

as an absolute dollar amount and as a percentage of market cap. ‘Brand

is an intangible asset, but it does have value and can be measured

[even though] it’s not on the balance sheet,’ says CoreBrand CEO Jim

Gregory.

Once CoreBrand has calculated a base level of BrandPower based on a

company’s revenue size and quality (as reflected in shareholder

value), this expected level of BEV becomes zero for the sake of

measuring changes that may result from a particular event, such as an

activist announcement. This explains why some companies show dips in

BEV percentage and dollar value to negative numbers. Because the

corporate brand contributes millions or even billions of dollars to a

company’s stock price and market valuation, any changes in it can have

a significant impact on stock performance.

Using a list of activist campaigns (provided by FactSet SharkWatch)

conducted against S&P 500 companies related to value creation, board

seat and CEO/officer removal announced since January 1, 2006,

CoreBrand analyzed 66 companies, all but eight of which show a clear

inflection point in their familiarity and/or favorability scores in

the year of the activist campaign.

‘We’re trying to identify inflection points that start a trend going

in one direction or another,’ Gregory explains. ‘It’s not necessarily

that activism is driving it – it may not even have caused the

direction – but it’s an identifiable point in time that brings

attention to an issue, and that attention can continue’ beyond the

activist campaign.

Eight of the 66 companies analyzed proved inconclusive, with

insufficient current data to see a trend, leaving a base of 58

companies in the study. Thirty-six (62 percent) of those reflect a

major inflection point of their corporate brand in the year of the

activist campaign; 15 (26 percent) show a small impact on the

corporate brand; and six (10 percent) indicate no impact from the

activist campaign.

Based on the results, CoreBrand finds that shareholder activism is

likely to have a significant impact on a corporate brand. Of the 36

companies with a large inflection point:

·

19 show significant long-term declines in favorability, indicating

perceived quality of the company

·

Seven show modest improvement in favorability

·

Two show improvement in familiarity, while favorability remains flat

·

Eight have mixed results showing short-term gains followed by declines

in the corporate brand.

The second conclusion reached by the research is that the impact of

investor activism on the corporate brand appears to be long term.

Third, the impact can be significant and longer-lasting on the

downward side, while the upside of investor activism tends to be

modest or short-term in nature. Fourth, even when there is modest

upside impact, the long-term trend is often negative.

Long-term decline in favorability

CoreBrand provided three case studies to exemplify various insights

about the impact investor activism has on brand equity value. Two of

the companies – Electronic Arts and Marsh & McLennan – are from the

group showing long-term declines in favorability, while the third

company, Family Dollar Stores, is from the group where there was

modest improvement in favorability.

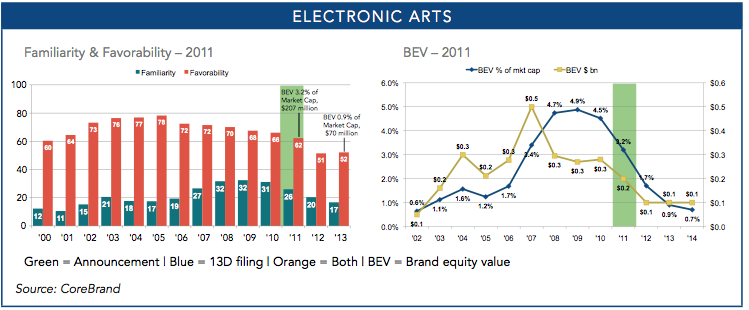

For Electronic Arts (see below), BEV as a percentage of market cap

declined from 3.2 percent to 0.9 percent and the value of the brand

plunged from $207 million to $70 million between 2011 and 2013. These

changes mirror declines in favorability and familiarity, as well as

revenue, even as the company’s market cap grew from $6.6 billion to

$7.1 billion over the same time period.

Declines in perception of management and overall reputation in 2006

overrode an essentially flat investment potential between 2006 and

2010 to initiate the overall decline in favorability. Erosion in

Electronic Arts’ brand from 2011 to 2013 identifies a failure of

management to see an opportunity to increase enterprise value by

adjusting through brand, CoreBrand concludes.

The name Electronic Arts has very low familiarity for a company whose

major brands, EA Sports and EA Games, are so widely known. The company

could have created billions of dollars of shareholder value by simply

changing its name to EA as early as 2006, according to CoreBrand. It’s

the corporate brand that matters when companies confront a proxy

battle, Gregory emphasizes.

Unfortunately, the details of the proxy battle announced in May 2011

by Relational Investors in pursuit of a board seat don’t seem relevant

to the drop in Electronic Arts’ brand value, which had already begun

in 2009. It could be that Relational, having witnessed a $641 million

loss in the fourth quarter of 2008, layoffs of 17 percent of the

workforce in late 2009 and other signs of trouble, saw weakness in

management that it believed it could exploit to win a board seat,

though why it waited two years is unclear.

The proxy fight, however, was reportedly undisclosed until a

settlement had been reached with Electronic Arts’ board, giving

Relational the option to place one director on the board. It’s

unlikely the activist campaign by itself caused the brand value’s

continued decline from 2011 to 2013, so there were probably other

factors.

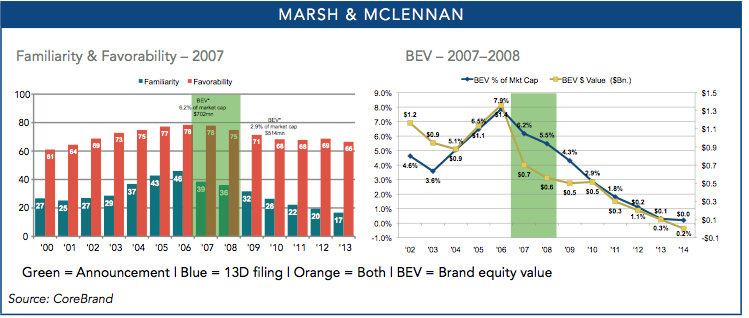

Elsewhere, Marsh & McLennan’s revenue declined slightly between 2007

and 2010, while market cap increased from $11.3 billion to $14.9

billion (see above). Both familiarity and favorability dropped and, as

a result, the BEV percentage of market cap fell from 6.2 percent to

2.9 percent.

Along with the decline in BEV percentage, in dollar terms, brand value

fell from $702 million to $514 million between 2007 and 2010, despite

a 31.9 percent rise in market cap. Had familiarity and favorability

not declined and had the company maintained its BEV at 6.2 percent of

market cap, the value of the brand should have climbed to $924 million

in 2010. Marsh is a case of creating shareholder value at the expense

of brand health.

Improvement in favorability

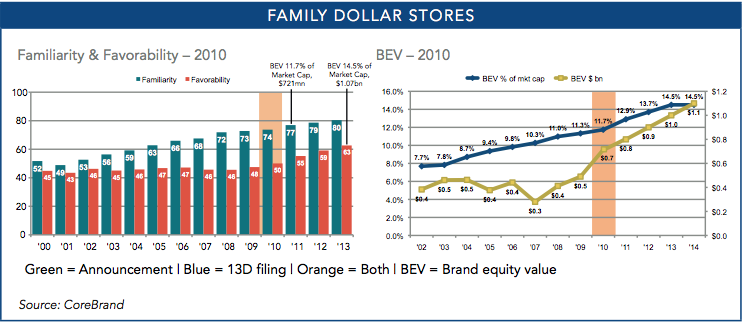

The third case study, Family Dollar Stores, demonstrates one of the

few examples where brand value improved as the result of an inflection

point in the year of an activist campaign. In March 2011 Trian Fund

Management made an unsolicited takeover offer for Family Dollar. The

company rejected the offer of $55-$60 per share and quickly adopted a

poison pill to protect itself from hostile bids. It later granted

Trian one board seat in exchange for a cessation of its takeover

efforts.

Family Dollar’s favorability score had begun to trend up from being

flat at 46 in 2007 and 2008 to 48 in 2009 (see opposite), at least a

year and a half before Trian made its move. But the uptrend became

more pronounced in 2011 after the hostile takeover bid and poison

pill, with favorability rising from 50 to 55 and continuing its ascent

to 63 by 2013. Similarly, familiarity – which had been inching up one

point per year between 2008 and 2010 – rose three points to 77 in

2011 and extended its gradual increase through 2013.

Looking at a breakdown of the three dimensions of favorability,

CoreBrand notes that investment potential had been gradually rising

from 2003 while overall corporate reputation, and perception of

management in particular, flagged. It’s possible that Trian’s 2011

announcement may have spurred subsequent growth, although the chart

indicates that the other two attributes were already in an extended

uptrend by 2010.

Mirroring the favorability trend, Family Dollar’s BEV percentage, in a

steady uptrend since 2003, had an inflection point in 2011, when the

uptrend steepened and kept rising until 2013 before flattening out at

14.5 percent. BEV rose from $721 million to $1.07 billion in the same

period. Family Dollar appears to be a case of well-managed shareholder

activism, where lethargy in favorability was ‘activated’ by what seems

to have been a well- orchestrated effort to create value and

ultimately sell the company, according to CoreBrand.

Rival discount retailer Dollar Tree offered to buy Family Dollar on

July 28 this year for an enterprise value of almost $9.2 billion, or

$74.50 per share, a 23 percent premium over the closing price on

Friday, July 25. The Wall Street Journal reported that the offer came

amid veteran activist investor Carl Icahn’s push for a sale of Family

Dollar and threats to replace the board after CEO Howard Levine

overhauled the sales strategy earlier this year.

Other effects

There are cases where BEV changes for a company don’t clearly track

its favorability trend. Marsh’s favorability stabilized at 68 points

in 2010 after falling from a peak of 78 in 2007, the year KJ Harrison

& Partners submitted a proposal for the 2008 annual meeting

recommending that the company spin off the Kroll and Mercer units to

enhance shareholder value. But BEV percentage continued to decline,

from 2.9 in 2010 to 0.2 in 2014, which suggests an even longer-lasting

adverse impact on brand equity value than the favorability change

indicates.

While favorability had stabilized, the continuing decline in Marsh’s

familiarity score from 26 in 2010 (compared with 39 in 2007) to 17 in

2013 seems to account for the continued drop in brand power, according

to CoreBrand.

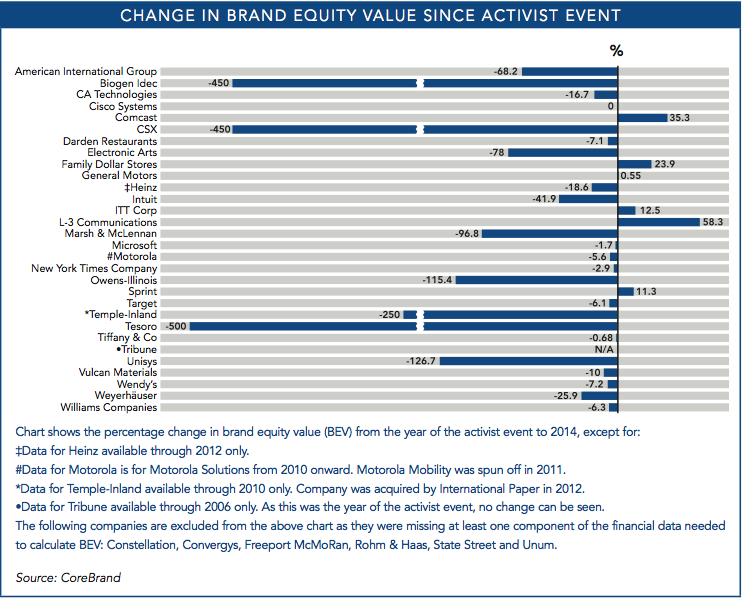

Weyerhaeuser’s BEV percentage continued to drop from 2006 to 2014,

even as favorability bottomed out in 2010 before rebounding by 2013 to

above its 2006 level. In 2006, Franklin Mutual suggested the timber

company modify its corporate structure to become more tax-efficient by

converting to a real estate investment trust. Like Marsh, the

subsequent decline in Weyerhaeuser’s BEV percentage appears to have

tracked along with familiarity, with the increase in BEV percentage in

2011 corresponding to a rebound in familiarity that same year.

A company’s familiarity score may fall after an activist event if, as

a result of the event, there are enough changes in corporate structure

or assets that business leaders surveyed are no longer certain what

transpired, says CoreBrand.

Fifteen activist campaigns for 12 companies led to proxy fights.

CoreBrand calculated average changes in familiarity, favorability, BEV

percentage and BEV dollar amounts for four groups of companies

according to the outcome of the proxy contest – management win,

dissident win, split and settlement/concession. Most of the averages

indicate declines in all scores. The only average gain is in BEV

percentage change for companies that settled with dissident

shareholders.

Biogen Idec was one of the few companies that had declines in

familiarity and favorability after the activist campaign announcement,

which may indicate the company stopped communicating after the

activist event. That’s one option a company can choose, especially if

it lacks confidence in its story – ‘but it’s a self-fulfilling

prophecy,’ warns Gregory. ‘If you don’t communicate, a negative will

fill that vacuum’, ensuring a decline in brand equity value.

More companies are paying attention to their CSR positioning, but

Gregory sees those efforts being wasted when companies don’t take care

to nurture their brand. Not only is that potentially costing them

customers and market share, but it’s also having an impact on employee

morale and media coverage. When corporate brand value is being

preserved, ‘you’re getting more positive stories from the media, and

not having to spend as much on PR,’ he concludes.

Copyright Cross Border Ltd. 1995 - 2014 All rights

reserved. |

|