|

Proxy Fights

Cost U.S. Companies $4.8 Million On Average

Posted By:

Michael Ide

Posted date: September 10, 2014 12:26:18 PM

Proxy fights have cost US companies an average $4.8 million so far

this year according to the latest issue of

Activist Insight, with

management consistently outspending activists for anything above

micro-cap stocks in what

activist investors say is a classic case of misaligned incentives, but

partially just reflects the two sides different obligations

Management spends

more on proxy fights than activists

As

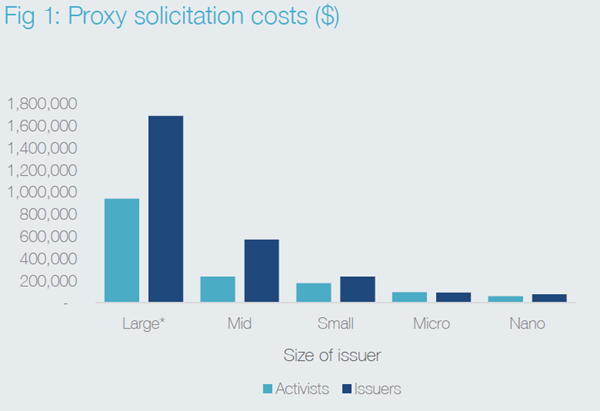

you would expect, the cost of a proxy fight goes up for both sides as

the market cap of the target company increases, but the jump small- to

mid-cap companies is still pretty striking, increasing almost

five-fold according to quarterly and annual reports. Activist Insight

points out that large-cap proxy fights are still pretty rare so the

sample size is small and the average could easily shift if large-cap

fights become more common.

The costs to activists also go up based on the size of the target

company, but not nearly as quickly. Going on proxy solicitation costs,

which both sides have to disclose,

activist investors are often

outspent by 2:1 or more.

“Defending irresponsibility requires a lot of effort,” says

Shareholder Forum chairman Gary Lutin, “but it will always be worth

spending whatever amount of other peoples’ money is required.”

That’s a cynical way to view the situation, but it’s not entirely

inaccurate either. Activist funds have a strong incentive to keep

costs under control so that the investment works out, while board

members playing defense in a proxy fight have more binary outcome that

doesn’t give them much reason to hold back. At the same time,

management has an obligation to give every shareholder the opportunity

to vote, and reaching out to a diverse group of institutional and

retail investors is labor

intensive and expensive. Activists only have to contact the handful of

institutional investors they think are likely to back them in the

coming vote. Experienced activists will also have more experience with

proxy fights and standing relationships with legal firms, PR, and

other professional service providers.

Proxy fights can

cause smaller companies to post losses

Even though the absolute cost goes down, small and medium-caps have to

consider the possibility that spending a few million on a proxy fight

will push them from black to red (to say nothing of micro-caps).

Activist Insight gives the example ValueVision Media Inc (NASDAQ:VVTV)

which spent $5.3 million unsuccessfully trying to fend of

Clinton Group, which spent

$800,000 to pick up four board seats and contributed to ValueVision’s

losses for the quarter.

|

Copyright © 2014 Valuewalk.com |

|