|

THE WALL STREET

JOURNAL. |

Business

Does IBM Love

or Hate Itself?

Stock Buybacks Make

Firms Look Attractive, but Also Deprive Them of Capital for Real

Investment

|

|

By

Dennis K. Berman |

|

|

Updated

Jan. 21, 2014 4:27 p.m. ET

There is a

rare type of organism that eats itself alive. One of them is

International Business Machines

Corp.

For the

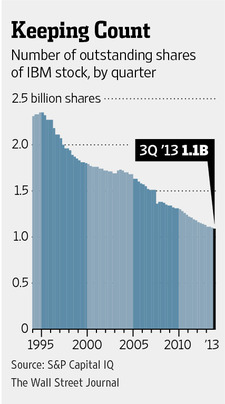

past 20 years, IBM has been an avid, methodical buyer of its own

stock. In 1993, it had 2.3 billion shares outstanding. Today it has

1.1 billion, shrinking at more than 1% per quarter over the past few

years. At that pace, there will be no more publicly traded IBM shares

left by 2034.

Rejoice!

You might regard all this buying as good news for shareholders.

Buybacks push up earnings per share. They flaunt management's

confidence in the future. And they are a reason why retail investors

have held on so lovingly to IBM stock.

Look

deeper at IBM and dozens of mature U.S. companies, and you can sketch

a different, more ominous, story: That CEOs are in fact stuck,

reluctant to build new plants, launch products or pursue an

acquisition.

By rote

and by fear, they are pitching their billions into buybacks, nearly $1

trillion from the 100 largest companies in the S&P since 2008. In the

12 months ending in September, the total dollar amount of all

corporate buybacks increased by 15% from a year earlier, according to

S&P Dow Jones Indices.

Cheap

money from the U.S. Federal Reserve helps sweeten this deal. And one

can't underestimate the threat from shareholder activists, who now

patrol the market like prison guards with billy clubs. Overspend and

get whacked.

Other

investment just hasn't materialized at the same rate. Among the entire

S&P 500, the median change in capital spending is 16.7% over the past

five years, based on a screen of stocks using Capital IQ data.

The danger

is that those buybacks have been substituting for substantive future

investment, be it software engineers, new products, or extra

marketing.

This has

two effects: It stymies the economic growth originally intended by the

Fed. And it could eventually leave businesses ill-equipped to adapt to

changes in their industries, especially technology-intensive ones.

Hewlett-Packard Co. pumped

tens of billions into (high-price) buybacks from 2003 to 2011 and is

now is struggling to find its way.

|

For the past 20 years, IBM has been an avid, methodical buyer of

its own stock. Bloomberg News |

|

IBM

competitor

Amazon.com Inc., meanwhile,

continues to pour in big dollars into actual technology. It grew its

capital spending 14-fold since 2008, and R&D spending fivefold.

Investor

Jim Chanos is starting to worry about just this problem. As one of

Wall Street's best-known short sellers, he's quietly been building an

investment thesis around the idea that buybacks are a sign of

corporate weakness, not strength.

Mr. Chanos

shared his analysis with me from a bright conference room in his

Midtown Manhattan office. We were both left agog at what the numbers

seem to show about how companies are allocating their dollars. Can

this really be right?

By his

count, for instance, the recent return on IBM's buybacks is about

6.5%. Not a terrible number. But IBM's return on what he dubs its "net

business assets"—actual stuff used in actual business—is far better.

It is 18.1%.

Wouldn't

this be a sign to immediately raise investment and shrink buybacks?

Maybe IBM

has concluded there is no better place to put its money. Or that it is

simply doing what stockholders want. It is hard to tell.

"Our

capital allocation model drives reinvestment in the business through

R&D, capital expenditures, and acquisitions, it pays the dividend

every quarter since 1916, and it returns excess capital to

shareholders through share repurchase," said IBM spokesman Michael

Fay. "We can do both, invest and return cash, and we do."

IBM is no

outlier.

Honeywell International Inc.

has been earning about 3.8% on its buybacks, according to Mr. Chanos's

numbers, compared with 13.4% on business assets. Honeywell spokesman

Robert Ferris said the company's total return—which combines

share-price appreciation and dividends—had outpaced its peers and the

broader S&P 500 over the past decade. During that stretch, Honeywell

has split cash flows roughly in two—between business investment and

returns to shareholders, Mr. Ferris said.

Oracle Corp.'s numbers also

showed a large split, between 4.8% return on buybacks and 32.1% on

assets. Oracle declined to comment.

"Corporate

CEOs, with their massive share-buyback programs are in effect

investing in the stock market rather than in expanding business

opportunities at their companies," said Mr. Chanos. "Either they

expect higher returns from the market, or lower returns in their

business, or some combination of both. Given their questionable track

record in timing the market, this may be a cause for concern."

Mr. Chanos

said he was shorting stocks based on this thesis. He wouldn't specify

which ones.

As for

IBM, buybacks still rule. It has raised the amount in recent years and

since 2007 has spent $60.4 billion. The company just made

announcements about new investments in data centers and its Watson

analytics product. But annual capital spending and research and

development have been roughly flat for nearly a decade, between $10

billion and $11 billion.

Many on

Wall Street are now beginning to regard IBM as a company more focused

on its stock price than its long-term path. "Only IBM knows what it

might be forgoing," says

Barclays analyst Ben Rietzes.

But "one can make an argument for organic investments," especially

with revenues shrinking 3% and fresh competition from cloud-computing

competitors.

This

question of investment isn't a conundrum just for IBM. It is for every

CEO protective of his job, unsure about the economy, and fearful of

the activists with the prison-guard eyes.

And so

here it is in 2014, five years since the worst of the financial

crisis. Are they playing to win? Or still playing not to lose?

Write to

Dennis K.

Berman at

dennis.berman@wsj.com and

follow on Twitter:

@dkberman

|